In their TED talk, Julian Pistone & David Steinacker shared the story of Kevin, a boy from rural Kenya. Kevin is an orphan and his cousin Sam pays for his school fees. Neither of the boys has a bank account, credit and debit cards.

Now think, how can you send money to your friends or family without a bank account?

Via the phone, this is what Kevin and Sam do. Both use MPESA — one of the mobile money companies in Africa offering money transfer service.

Kevin’s story isn’t unique. There are hundreds of thousands of similar cases across the African continent. People and businesses need secure technologies to store cash, make transactions, grow capital.

For instance, Airtel Money helps small-scale entrepreneurs in Uganda, Mobisol provides families in Tanzania with electricity and the ability to accept payments through mobile providers.

Africans say it’s innovation, the real innovation that turns their lives for the better.

Let’s talk about this.

What you will learn from today’s post:

- discrepancies of the mobile money technology development in African countries;

- the impact of mobile money on African economy;

- payments-as-a-system – key trend;

- GSMA’s project to combat financial exclusion in Africa.

Mobile money in Africa: stages of development

We’ve already shared our take on digital financial services and mobile money interoperability in emerging countries.

The industry is young, yet it has already greatly contributed to solving the poverty, low standard of living and financial illiteracy problem all across the continent.

A quick glance at the African mobile money industry:

- over 469m registered and 181m active mobile money accounts;

- the total value of transactions in 2019 was about one third higher than in 2018;

- sub-Saharan Africa is outrunning South Africa in terms of the expansion of mobile money services;

- there are 137 service providers in Sub-Saharan Africa comparing to 18 in Middle Eastern and Northern regions;

- mobile-money transactions in Central Africa increased by almost 50% even though Central Africa has huge regulatory issues;

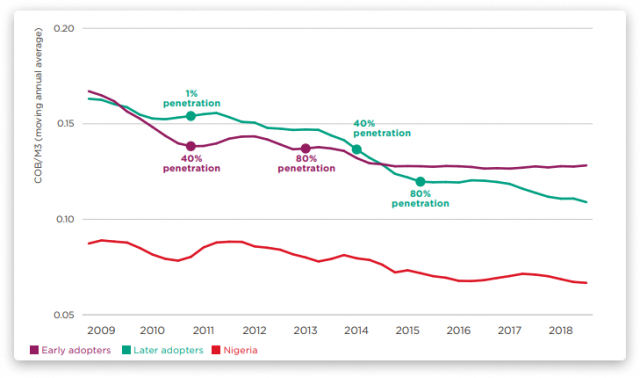

- COVID-19 appeared to be a huge driver for facilitating digital money transfers across the continent and forced BCEAO to make financial transactions more affordable;

- super apps offering a combo of services to Africans are under development.

There are five agents taking part in a typical mobile money value chain:

- Deposit holders

- E-money issuers

- Agent network operators

- Payment service

- Telecom providers.

The functions of each player can be fulfilled by either banks or FinTech companies.

“ Who does what” determines the mobile money operating model and the development stage of the country or region. Those stages are three: emerging, growth, and maturity.

1. Emerging

There’s a lot of cash in the circulation in these countries and agents are an integral part of any transaction. This increases the cost per transaction and decreases the profit margin.

EY suggests that investors moving into this niche take a dive deep into the local market and understand all the risks.

Countries at this stage: Senegal, Togo, Zimbabwe.

2. Growth

At this stage, mobile money services are constantly expanding and the market sees high rates of consumer adoption. Plus, competition among providers becomes very fierce.

The profitability of transactions grows and marginal cost approaches zero. For investors, it’s a great opportunity to get lucrative returns; but choosing the right model may be a challenge.

Countries at this stage: Mozambique, Ghana.

3. Maturity

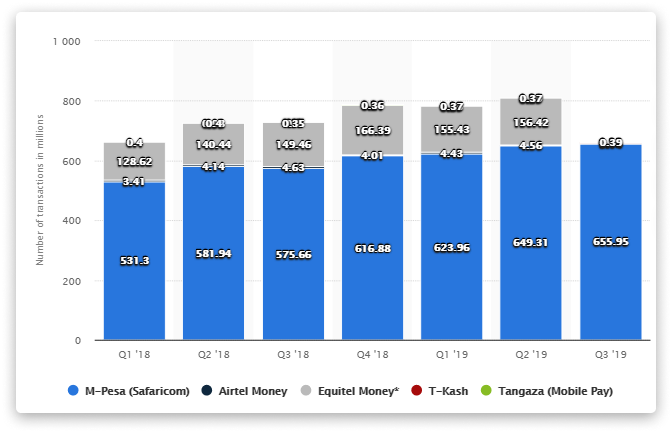

In countries like Kenya, there’s usually one or several frontrunners — mobile money services providers.

The widespread usage of mobile money transforms it into a new quasi-currency and the majority of transactions take place within the network.

Investors may find some opportunities to generate capital with standard returns and risks.

Countries at this stage: Kenya

Mobile money impact: Africa’s monetary and financial stability

Ugandans from the YouTube IFS video are telling about the benefits Airtel, leading mobile provider, delivers to local businesses and individuals, in particular:

- facilitation of supplier-consumer payments;

- secure storage for cash;

- usage of e-money to pay utility bills;

- easy and fast money deposition and withdrawal;

- ability to supplement to Airtel as an agent and gain extra capital;

- improvement of financial literacy through training programs and education for agents;

- and the expansion of products range from money transactions to deposits and insurance;

- elimination of the financial exclusion gap in rural areas thanks to the service expansion.

The technology gives perks to every link in the chain:

- Users and households can manage cash flows better, which creates demand and provides smooth consumption.

- Businesses, in their turn, get an opportunity to build capital and create new offerings.

- The total income to the governmental budget grows and resources to support education and utility sectors multiply.

In the global sense, mobile money can have a significant influence on the monetary and financial stability for African countries.

Negative or positive? Here’s a spoiler: positive.

In 2018, GSMA published a detailed report with their findings on how the innovation impacts macroeconomic and financial development — the main objectives of central banks.

Here are a few takeaways.

1. Mobile money and inflation

On the one hand, mobile money can increase firms’ ability to make productive investments, and therefore cut prices. At the same time, new money brought to the system creates wider credit opportunities, stimulates more productive investments and, again, are to cut prices.

On the other hand, the more money consumers have, the more they can consume. It may lead to excess demand for goods/services and rising inflation.

Only practice and time can show the real outcome, so let’s just wait.

2. Mobile money and monetary policy

The monetary policy of any Central bank, including African regulators, aims to control the money supply and set interest rates. By doing so, regulators achieve price stability.

If mobile money increases the amount of currency in circulation (e-money is considered as a cash substitute in this case), the money multiplier will grow.

It means that there will be more broad money relative to the money base, whose tiny change may influence the money supply.

The regulator, in its turn, can control a greater share of economic activity, influence investment decisions and, therefore, price stability.

3. Mobile money and financial stability

Some experts warn that mobile money can create additional systematic risks to the entire banking system.

Others predict that it won’t happen since the technology refers to a payments service meanwhile actual deposits are saved on trust or escrow accounts.

In this case, local shocks won’t be transmitted to the country’s banking system.

And others worry about the future of incumbents — mobile money can displace traditional banks, which may shift the balance.

But there’s the third scenario, a more optimistic one. Mobile money providers and banks in Africa are developing, each in its direction. Since the first aren’t prudentially regulated, these companies can’t offer bank deposits or credit services.

Um, what about Airtel?

They partner with Maisha Microfinance Bank to provide a savings and loan mobile money solution.

So, service providers can take a piece of the incumbents’ pay only through allying.

Those people and businesses who are unbanked remain unbanked, yet with access to convenient mobile payments.

Regular bank clients are likely to continue using traditional bank products.

Payments as a platform — the future of mobile money in Africa

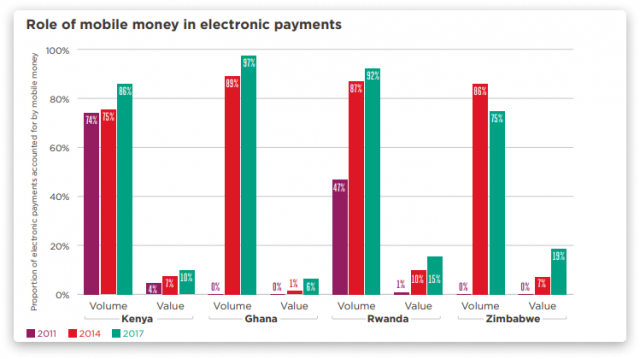

Over a decade of unprecedented growth, mobile money became the leading payment platform for the digital economy in emerging markets like Africa.

There’s no need to hit industry reports to understand the role of mobile payments for an average African.

“We feel the positive impact of mobile technology in Kenya”

“Africa is thankful. Perhaps more changes are yet to come”

“Great product, this is what we need more of”

This is what people from Kenya, Tanzania, Uganda and other countries say about mobile payments as a platform.

GSMA believes that the key question today is how the technology will evolve to support the needs of all parties: users, providers, the government.

The platform approach is what may work the best. It will let agents generate additional revenue, promote employment and economic growth.

In November 2018, Orange Group and MTN Group announced the launch of Mowali (Mobile Wallet Interoperability).

Mowali is an example of payment-as-a-platform solutions designed to simplify the deployment of payment and mobile money transfer in Africa between operators.

Once after the launch, Mowali brought together over 100 million mobile money accounts and mobile money operations in 22 of sub-Saharan Africa’s 46 markets.

The benefits of using Mowali for agents:

- One connection. It’s easy to connect to the platform: implement APIs, test how it works in the sandbox and switch to production.

- One contract. Open a settlement account without the traditional hassle: pass CDD checks and sign the contract.

- One settlement. You get clear info on your debt and credit daily from your account.

Mowali features:

- local and international money transfers;

- online and merchant payments

GSMA fighting mobile money challenges in Africa

From a group established to design a pan-European mobile technology to the global representative of mobile operator and organizer of industry-leading events – it’s a brief history of GSMA.

Key initiatives of GSMA lie in mobile technology and its power to foster:

- future networks (5G and RCS messaging);

- identity (log-in solution Mobile Connect);

- the Internet of Things (connected drones, smart manufacturing, road safety)

- mobile for development.

At the beginning of 2020, we collaborated with GSMA working on the Interoperability Test Platform MVP project.

The organisation is planning to launch the first jointly test platform to test the GSMA Mobile Money API and Mojaloop.

Mobile money interoperability is crucial to support the ecosystem where users can send and receive money through the network.

GSMA created a dedicated Inclusive Tech Lab working on the first free and open-source Interoperability Test Platform.

The project goal was to prove the concept of the platform. Developers, the end-users, get access via API hub to simulators which are used to simulate mobile operators and audit providers.

Simulators were used to simulate mobile operators and audit providers. We used an open-source API hub. The end-user will be developers from service providers and mobile operators; inter-communicating.

We managed to build an MVP under two months and released version 1.0 after 4 months of the project.

Afterword

We are on the threshold of the African economic miracle driven by new shapes of an oldie but goodie mobile payments.

Initially emerged as a handy service for mobile money users in Africa, now mobile money has evolved into a complex payment infrastructure.

- To unbanked African population, it provides wider opportunities for financial management and improves living standards.

- Startups and businesses also find benefits in accelerating B2C and B2B payments and gaining access to the loan market.

- The perks will also accrue to incumbents, financial institutions joining the platform. They get a chance to participate in the digital economy and boost the economic growth of local markets.