Did you know that online purchases, mobile payments and personal wallets are not available for the majority of people in Mexico, Brazil, India or Nigeria?

According to UBS, almost 1B people in emerging markets don’t have a formal bank account.

Those who are not excluded from the digital finance services (DFS) industry typically have access to basic functions. It leads to a significant amount of cash in circulation and high fees, and individuals can’t reap the benefits of personal investments and have limited access to loans.

The adoption of mobile digital financial services (DFS) might be the first step to solve the problem. For example, money wallets available at fingertips are to help citizens in developing countries eliminate theft-related risks and make effective investments.

The World Bank, McKinsey and other organizations research this complex topic from the economic and social point of view compiling detailed reports on the progress and solutions in the domain of DFS. While it’s difficult to stuff everything in one article, we’ll try to cover the basics of online digital financial services for you to be kept in the loop.

What are the digital financial services?

McKinsey defines digital financial services in the following way:

DFS is financial services delivered over digital infrastructure—including mobile and internet—with low use of cash and traditional bank branches.

The digitized national payment infrastructure includes types of DFS, digital channels (mobiles, computers, cards used over point-of-sale (POS)) and users (individuals, businesses, and government entities).

65% of adults in transitional economies lack access to basic financial services available on smartphones. And what’s more important, not only the poor but the middle class as well.

People in rural areas and women are particularly affected, which significantly reduces their standard of living.

Financial inclusion (decreasing the number of unbanked people) together with financial application development has a huge influence on the global society and economy at the macro- and micro- levels.

Individuals get a chance to invest in housing, health, education and achieve a better standard of living. Plus, they become less vulnerable to an emergency situation such as a job loss.

At the macro-level, a shift from cash to online payments is to increase the country’s GDP and facilitate economic growth.

The COVID-19 expansion has fostered many FinTech firms worldwide to speed up the development of brand-new solutions to provide appropriate conditions for social distancing and market changes.

The economic and health crisis has unveiled the benefits of DFS and their role in supporting sustainable growth.

Benefits of the financial inclusion according to the World Bank Group and McKinsey

- mobile money and payments can help improve people’s income earning potential and eliminate financial risks;

- the supply of DFS is to lower administrative fees;

- a wider range of services may foster personal investments and improve savings management;

- the adoption of DFS in emerging countries is aimed at building stronger institutions with less corruption;

- rules and policies created in the response of the DFS boom contribute to personal protection and reduce the cases of fraud;

- the more people will be included in the financial system, the higher level of financial literacy developing countries will have;

- innovations into local FinTech companies result in the growth of the global economy.

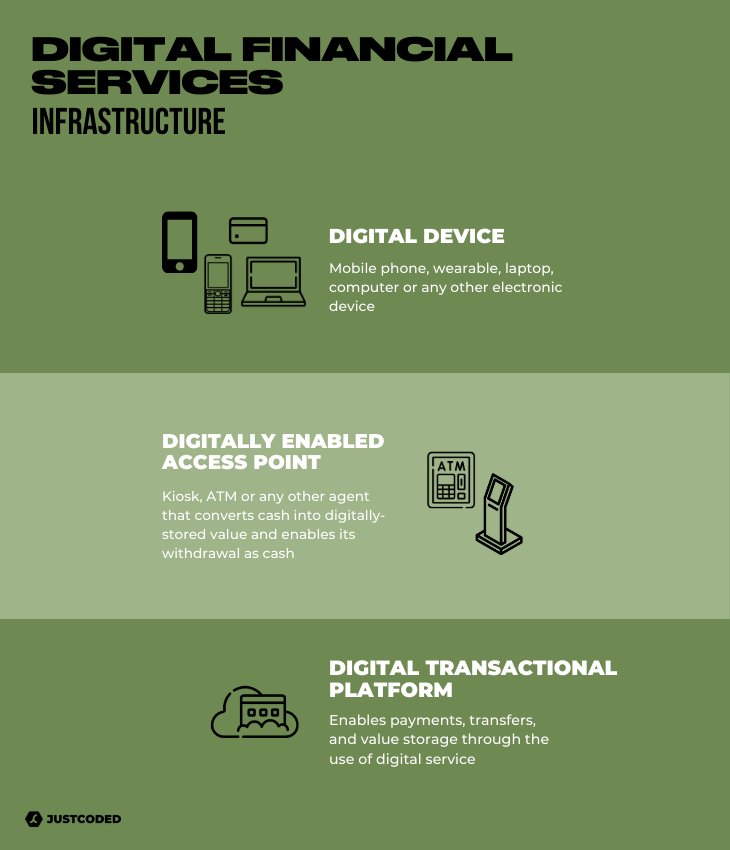

Types of digital financial services

All the products offered by mobile banks and alternative finance providers can be divided into 3 groups:

Savings and investments. First off, we’re talking about different investment instruments and opportunities: securities, mutual funds, crowdfunding platforms. Also, automated services based on AI/ML technologies can provide advice for portfolio generation and risk evaluation.

Payments and transactions. Some e-commerce platforms issue their e-money and enable clients to securely send small sums within their apps. Some FinTech firms are working on cross-border remittances. For instance, TransferWise and MFS Africa, have created an ecosystem uniting local payment infrastructures and e-money providers from different countries taking part in a transaction. As a result, TransferWise offers cheaper international money transfer services.

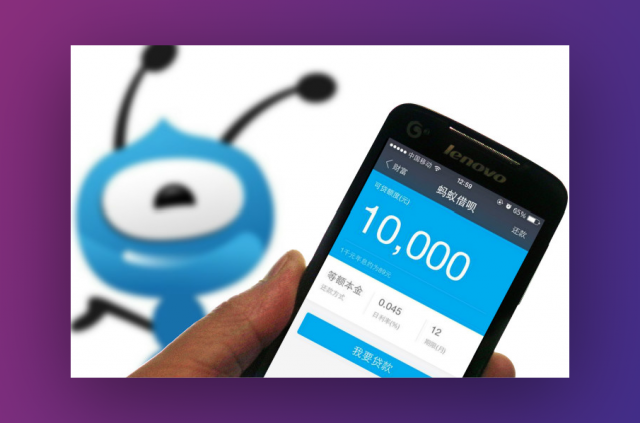

Individual and business loans (factoring). Again thanks to machine-learning technologies, millions of households now have access to financial help. Innovative algorithms make it easier and faster to collect data from socials, smartphones, other applications and analyse the borrower’s credit risk. For example, Ant Financial, an affiliate company of the Chinese Alibaba Group, provides loans in a matter of time: loan application and approval takes less than 10 minutes.

The now and the future of digital financial services: country experience

Let’s look at how different countries with emerging markets manage financial exclusion and help the unbanked population.

The World Bank in their new report on DFS (April 2020) divides all developing countries into 4 categories by the extent of DFS usage and adoption.

Ghana

Currently, the country is at Stage 1 and citizens have access to basic functions like payment transactions and personal accounts.

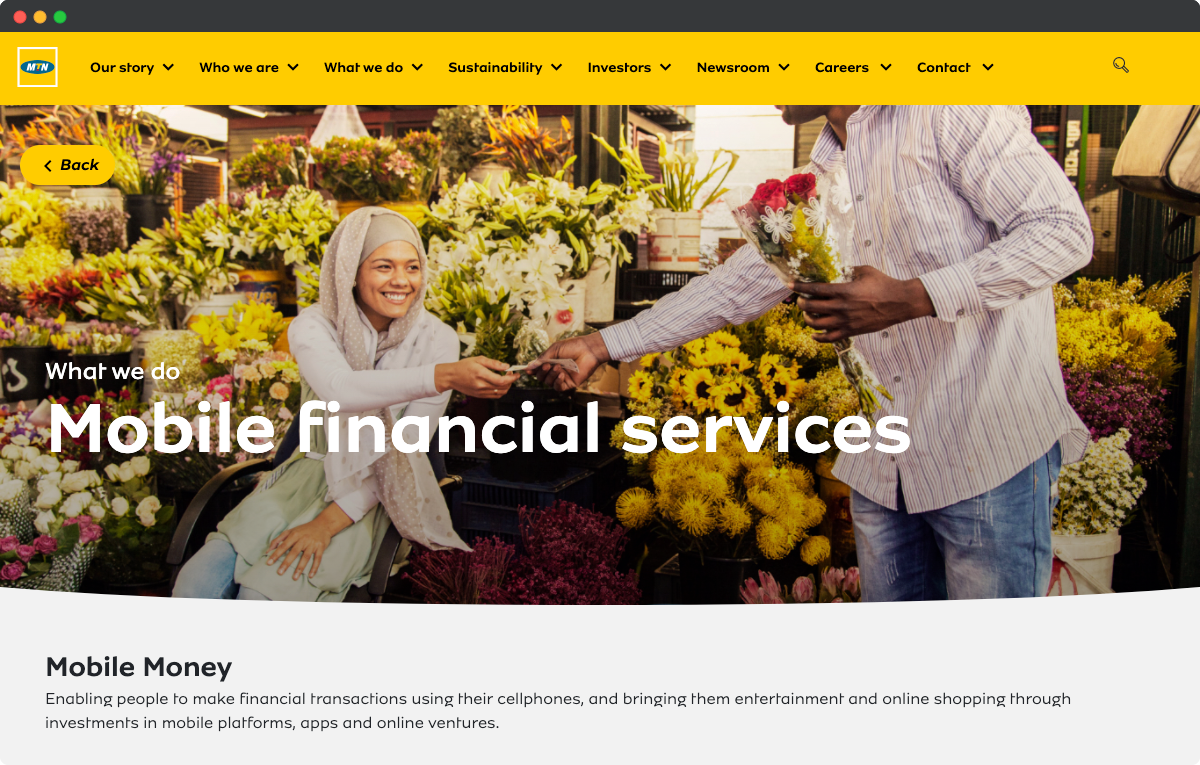

The crucial factors that positively impacted the financial situation were non-banks and mobile network operators issuing e-money.

For instance, MTN and PAYGo solar payments received permission to carry out payment transactions with mobile money.

In 2018, the Government took the next step towards DFS adoption. It created an interoperability system to connect mobile money providers and banks and enable transactions between different mobile money companies.

Also, with the support of the World Bank, Ghana has presented a new e-payment portal to serve governmental organizations.

India

India’s success is based on two pillars: digitization of G2P payments and a significant increase in the volume of payment transactions. To compare, in 2014, 53% of the adult population in India had access to bank accounts, in 2017 this figure was 80%.

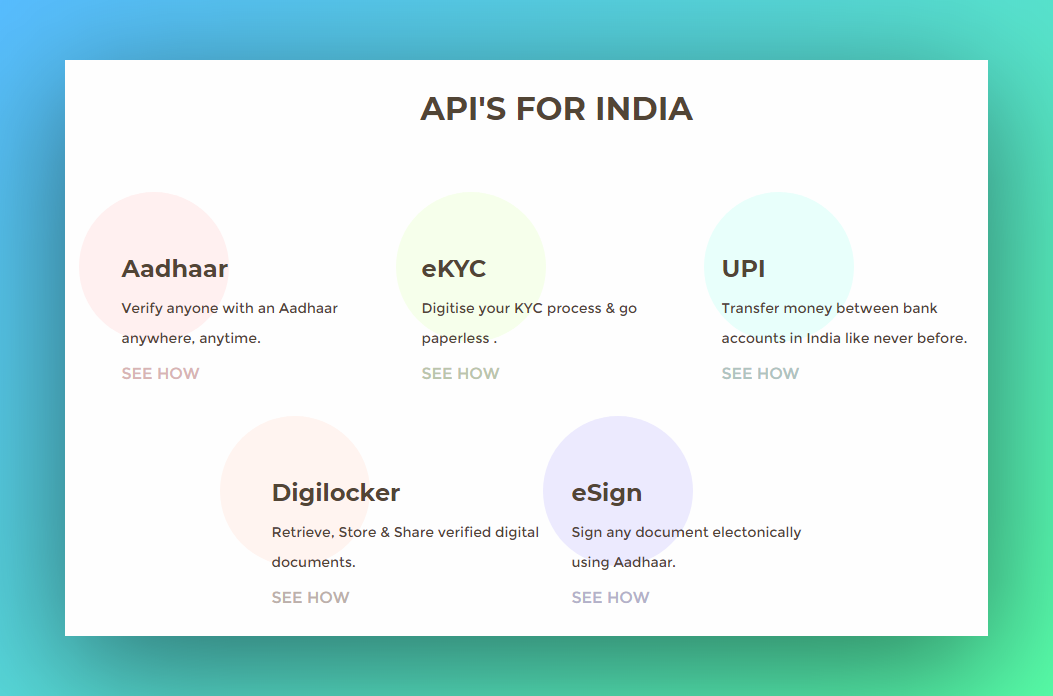

In 2009, India kick-started an innovative biometric identity program (Aadhaar) with a focus on simple identification method that helps companies pre-vet clients before they open a bank account. It greatly reduces the costs of KYC checks.

Another driver was The “India Stack”, a set of APIs on top of the Aadhaar system that includes eKYC, UPI, Digilocker and eSign.

The main goal of the program is to let all the parties (governments, businesses and IT companies) develop solutions to make service provision paperless and cashless.

Kenya

It’s a great example of scaling up from pay-as-you-go solar panels repaid via M-Pesa transfers to more advanced services like micro-finance and general-purpose loans.

Kenya is the leader in accelerating FinTech solutions among African countries. Here are only a few examples of successful DFS startups from Kenya:

- M-PESA for retail (merchant) payments;

- mobile-only retail bond, M-Akiba for micro-investments in governmental securities;

- the Branch app for providing digital loans;

- FarmDrive, a Kenyan data-analytics company helping agricultural companies increase their portfolio.

China

It’s the brightest representative from quadrant #4. China has a very strong ecosystem and, unlike other countries, its middle class roughly equals the population of Europe.

Thanks to a great number of local tech firms, intelligent specialists and incumbents, many challenges that emerging countries are facing now were successfully overcome.

Alibaba, the largest marketplace in China, launched its payment system Alipay in 2015. Now it has 451 million annual active users and processes over 153 million transactions every day.

Tencent, Alibaba and Baidu created an alliance and established WeBank in 2016 to provide small and medium businesses with business loans.

What’s important, non-banks and alternative financial services providers get permission from the regulator to use official credit registry.

It helps them build more accurate scoring models.

Challenges for banks and FinTech companies and growth opportunities

It seems like the authorities of developing countries have a given a green light to FinTech startups and the evolution of DFS. But there are still challenges slowing down this process.

Key challenges

- the population has low earning potential and lacks financial literacy;

- a poor regulation framework to control traditional and alternative financing;

- underdeveloped tech ecosystems and infrastructure;

- high compliance and risk management costs;

- limitations on trading and other financial activities;

- the domination of state-owned financial organizations.

Growth opportunities

- enabling new players, approaches and models such as AI/ML, Data/Cloud platforms, mobile technologies;

- opening the DFS market to non-banks;

- advancing the regulatory system towards better client protection;

- creating further demand for DFS and expanding their availability;

- removing barriers for new entrants to the market;

- large-scale G2P digitization.

Application of digital financial services: GSMA interoperability test platform

Now when the role of digital financial services and technology platforms in emerging economies is clear, let us show you one amazing project we were privileged to take part in.

The idea behind it is great, and we dare say, it can make the future of the DFS industry bright and better.

Our client, GSMA, has created a unique mobile ecosystem uniting mobile services providers, software companies, Internet providers, and device makers from all over the globe.

The cornerstone of the GSMA’s new project is mobile money interoperability: different providers and operators from various countries can interconnect their tech platforms via Mobile Money API and allow people to send and receive money via mobile devices.

In the global sense, it can help combat financial exclusion in African, Asian and Latin American countries.

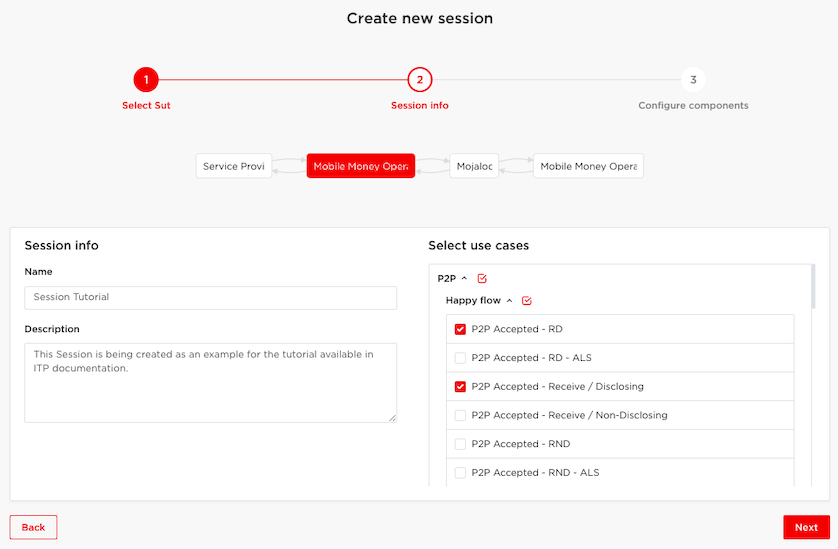

The interoperability test platform that is being created by GSMA is a one-of-its-kind solution based on GSMA Mobile Money API and Mojaloop.

Using the platform environment, ecosystem participants can test interoperable mobile money solutions across different use cases.

Currently, the platform is fully open for usage and contribution since it should undergo careful tests to be presented to the wider audience.

You can get access to the Interoperability Test Platform to test the behaviour of your system in different scenarios and test certain use cases.

The tech stack deployed by our team includes Mojaloop, GSMA Mobile Money API, Laravel, Vue.js, Amazon Web Services. Learn more about the project from our portfolio and on Clutch.

Epilogue

Financial services have great power. They can help a woman in Bangladesh who was retrenched and a small tourist business in India suffering amidst COVID-19.

Unfortunately, there’s still a great number of the unserved people who rely on cash and have no ways to augment personal capital.

Meanwhile, some countries are making important steps towards solving financial exclusion, others are not doing so well.

The key aspects that require changes to boost DFS are regulation, tech ecosystems and infrastructure, alternative finance providers, people financial education and literacy.