So, you’re here calculating the budget for your new project — a custom crowdfunding platform, for instance.

Everything seems clear: the scope, design & development costs, infrastructure and software deployment, third-party licensing.

You find a great tech partner, set the budget, stick to it.. and suddenly exceed it. How come?

Everything seemed to be taken into account, everything except for those nasty expenditures.

Post-launch costs, brand registration and certification, tech debt — to name a few.

In this article, we’re reviewing obvious and not so obvious hidden costs accompanying fintech software development.

Forewarned is forearmed.

5 things breaking your custom development budget

Our experience has shown that the below expenditures may burgeon your dev budget to enormous levels.

1. Server capacity

By default, fundraising platforms are complex web applications with a lot of embedded components and third-party integrations.

There is a linear dependence between the project scope and cloud server requirements.

Features like liveness detection may require servers with large processing capacities, which may be a substantial financial burden.

So if you’re considering scaling your platform up and expanding your business, eventually, you’ll have to move to new Amazon instances or Google Cloud virtual machines to make sure your platform is still stable and robust.

How to choose a suitable server capacity and optimise your budget? Only an expert DevOps specialist can answer this question. However, there are basic points you can start with: bandwidth requirements, IP address requirements, computing power requirements (CPU and RAM performance), volume requirements.

For example, GlobalGiving all in on AWS with 100% of its web traffic powered by AWS services.

It helps the company meet the demand globally, respond quickly to all user requests and load the website fast.

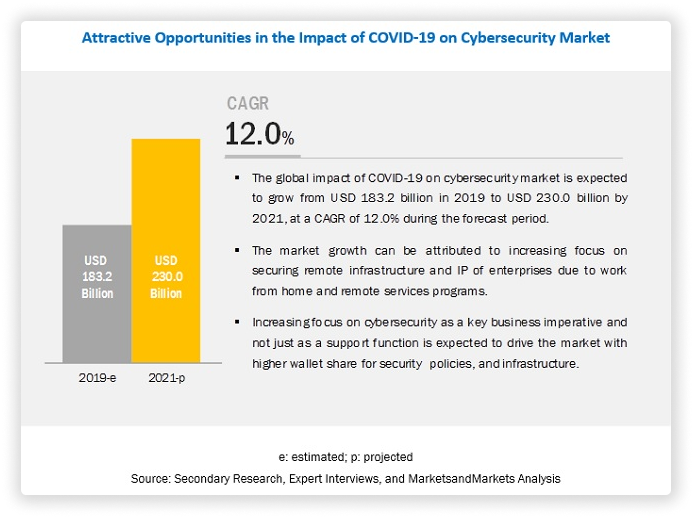

2. Data security

For cybercriminals, COVID-19 became manna from heaven. Cyber attacks were most prevalent in the healthcare and financial industries.

According to Verizon, in 2020, web application breaches accounted for 43% of all breaches and have doubled since 2019.

It means that FinTech companies should increase their security budgets to:

- implement innovative security technologies (AI/ML, cryptography, advanced identity and access management technologies);

- comply with data privacy regulations (GDPR, CCPA, LGDP);

- run regular internal and external security audits; in some cases, they need SOC2 certification.

According to AICPA, FinTech companies fall under the definition of a service organisation. Since crowdfunding companies sell services and expertise, your customers may ask you for SOC 2 report proving that your security controls protect data confidentiality, integrity, and privacy.

The average price for SOC2 report has a starting range anywhere from $30,000-$100,000.

3. Tech debt

It’s still a question what’s worse for a crowdfunding company — having a financial or technical debt?

Tech debt/code debt is the practice of relying on temporary easy-to-implement solutions to achieve short-term results at the expense of efficiency in the long run.

In simple terms, if your platform architecture and code has plenty of breaches, inconsistencies once made for the sake of marketing the product faster or issuing a release, you’re in tech debt.

And paying it may be a thorn in your side.

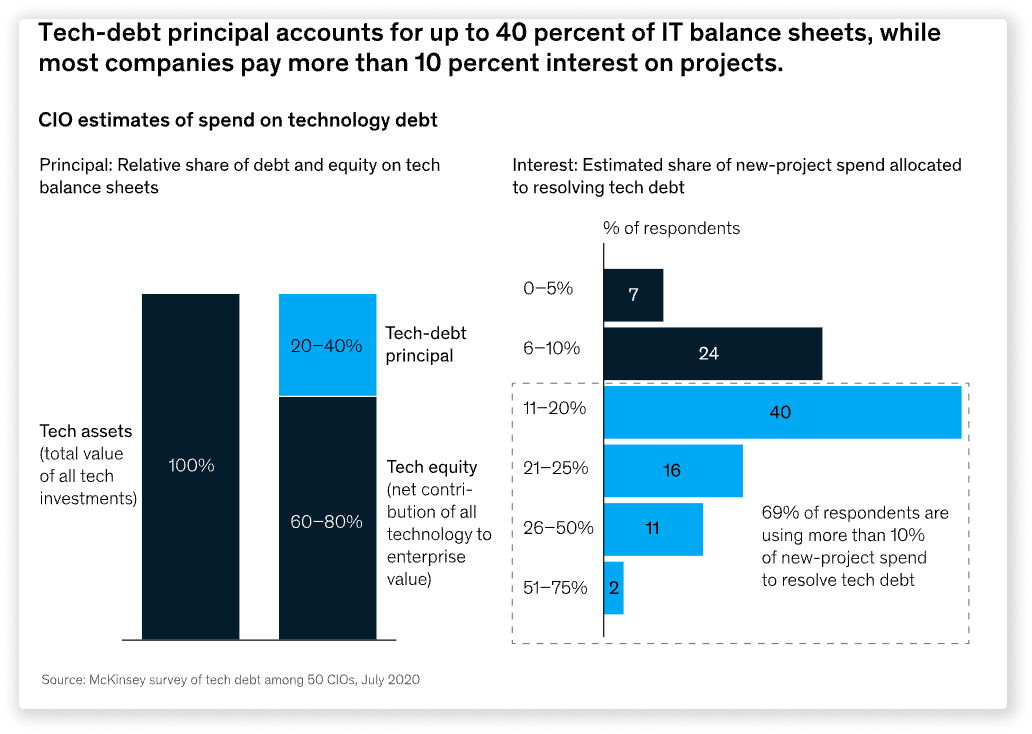

McKinsey reports that every technology company has some tech debt, and it increases with every modernisation made to its corporate systems.

Companies tend to pay 10 to 20% of the technology budget to resolve the issues related to the tech debt.

If not treated properly, the debt is growing and finally amounts to hundreds of millions of dollars

How to pay the tech debt accumulated in your crowdfunding project?

- Get rid of unnecessary apps and databases;

- simplify application interfaces;

- modernise technology to support current architecture;

- optimise the workload of the team: direct 25% of the time to solving tech debt issues.

4. Custom crowdfunding platform maintenance

You don’t pay for development, and you pay for the product maintenance. And it’s partially true.

Continuous support and maintenance (third-party API updates, code refactoring, server-side updates and regular backups, bug fixing, environment configuration) export your project money.

There are several product maintenance models:

- pay-as-you-go: you’re charged according to Time and Material model;

- proactive maintenance: reengineering and code refactoring;

- ongoing support: the dev team is available on call, usually at a higher price.

We at JustCoded offer support & maintenance to keep your solution abreast with new demands, technologies, and trends.

Our support package includes:

- product consulting on the post-MVP to reveal bottlenecks and suggest solutions;

- ongoing development by the dedicated team responsible for minor issues and major updates;

- UX and UI improvements once the early feedback is received.

We don’t have an established price for maintenance backing as every crowdfunding project has a unique business flow.

5. Integration with third-party services

No custom crowdfunding platform can live without integration with third-party services, unless you’re developing your own payment gateway, identity verification module, digital signature component.

Of course, you can do it, but what for?

Typically, third-party vendors provide paid subscriptions or licenses.

However, there are those charging for every transaction or a request sent to the database. KYC service and liveness detection providers stick to this pricing model.

Therefore, an increase in the client base, transactions, campaigns and deals may eventually lead to higher service fees.

Or the provider may update their pricing policy like PayPal recently did.

Before choosing a third-party provider, carefully investigate their pricing model and contract terms.

Typically vendors offer to fill in the client form and get a personalised quote.

We’ve got a good piece on the best payment gateways for crowdfunding sites and their fees.

Are there any other budget pitfalls?

Sure, you should be aware of:

- cost of brand registration and certification in your country;

- team expansion as a result of continuous scaling;

- client support price;

- future integrations and product versions (mobile app);

- tech and legal docs preparation.

How can you cut development costs with LenderKit?

Frankly, every other blog post on this topic aims to promote the in-house turn-key solution or service capable of building a custom website/platform from scratch. Ours isn’t an exception 🙂

But not every other blog post honestly answers the question “What’s cheaper — build vs buy?”.

On average, companies spend at least $102,000 (89,000 EUR) to build a crowdfunding platform.

In some cases, it’s better to do all the dirty job yourself. If your business model is sophisticated, technical requirements are complex, and you have plenty of time and a large budget for development, then you may risk and opt for the DIY approach.

If you need to pitch the idea to investors or market the product fast, your functional and non-functional requirements are standard, then your go-to may be LenderKit.

LenderKit is a white-label software for different types of crowdfunding businesses: equity investment platforms, p2p lending portals, real estate crowdfunding sites and donation-based fundraising companies.

It helps to automate capital raising cycle operations, streamline customer interactions and deal management.

LenderKit is suitable for both starting businesses and established companies.

What’s under the hood?

Main components and features:

- Marketing site layout;

- Investor portal;

- Powerful back-office;

- Investment flows;

- Fees management;

- 3rd party tools integrations;

- Built-in secondary market;

- Permission settings;

- e-wallets.

A mobile app for investors as a bonus.

Basic and Professional packages deliver the best cost for value to early-stage businesses whose objectives are: compliance with the regulatory requirements, prototyping, testing business assumptions, etc.

Established companies willing to expand globally or set a local crowdfunding portal may find Enterprise plan more appealing. It comes with more customisation options, integrations and premium post-launch support.

A great bonus is that we provide a source code bundle to our Professional and Enterprise clients.

Having all the numbers at hand, you’ll be able to take a build vs buy informed decision.

Bottom line

Okay, let’s sum up what we’ve got about the unpredicted costs of fintech software development.

- At the planning and budgeting stages, it’s very hard to get a sharp budget estimate. There are grey areas, and owners as well as tech partners may skip changes in the server infrastructure, changes in third-party vendors’ pricing, tech debt, advanced security measures, functionality scaling.

- “Buy” is cheaper than “build” — not always. The cost depends on your business type, project requirements and resources. Sometimes fine-tuning a ready-made solution takes way more time and money than if you build it from scratch.

- Our suggestion is to do deep research and investigation of development case studies and best practices that take place in your domain. And, of course, select a reliable and expert tech partner.