The idea of becoming landlords and gaining rental income has been always popular in the UK and other countries around the world.

In the 1990s-2000s the buy-to-let (BTL) market flourished and thrived with wealthy individuals and companies owning property portfolios.

Although ordinary backers were left behind and didn’t consider rental accommodation as an additional income generator.

Everything has changed after the updates of legislative taxation base regulating first-home and second-home purchases in 2017.

Something has to fill the void created by homeowners exiting the market. And experts found the way — buy-to-let crowdfunding platforms.

Our today’s task is to show you how buy-to-let crowdfunding works and what opportunities it promises to companies and their clients.

A sneak peek into buy-to-let crowdfunding

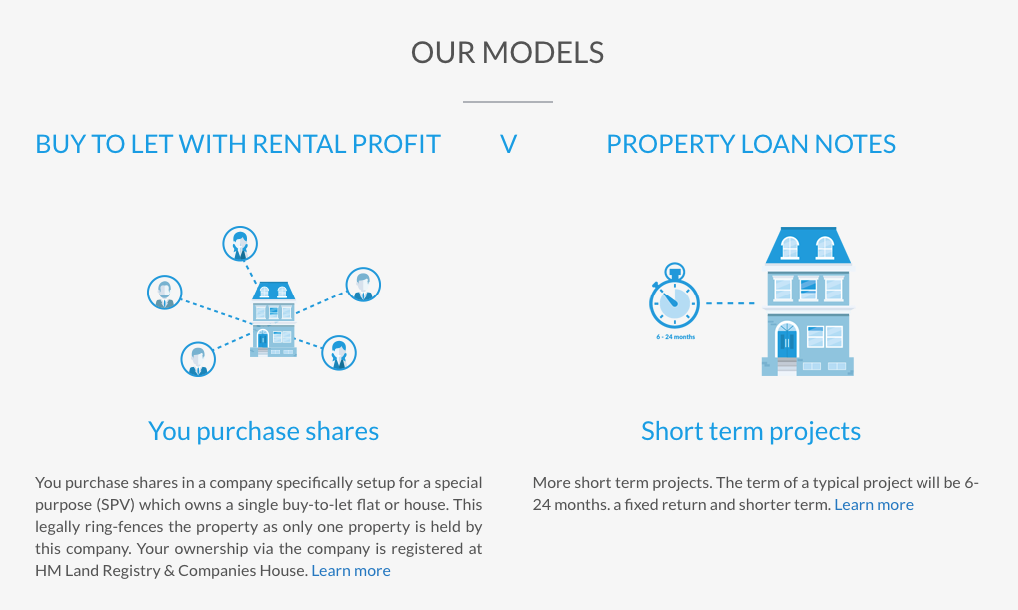

BTL deals in crowdfunding are as simple as ABC: investors pour money into a property project that they would rent out in the future. Shareholders get the portion of the rental income or can resell their investment later on the secondary market and gain extra capital.

Landlords aren’t involved in property management, and they don’t liaise with tenants – platforms hire agents responsible for this job.

Buy-to-let investments disrupted the property landscape once before.

The introduction of the Housing Act in 1988 led to a skyrocketing increase in volumes of buy-to-let loans. Before, these investments were only the prerogative of professional backers who had enough funds to get this opportunity.

The Act ensured landlords that tenants could occupy the rental apartment only for a specified period. Earlier, the tenants could stay in a property indefinitely and even pass down this right to relatives (wow!).

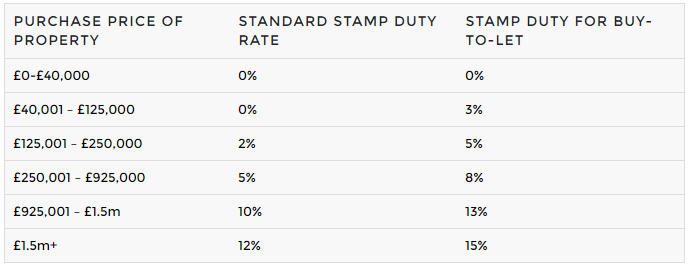

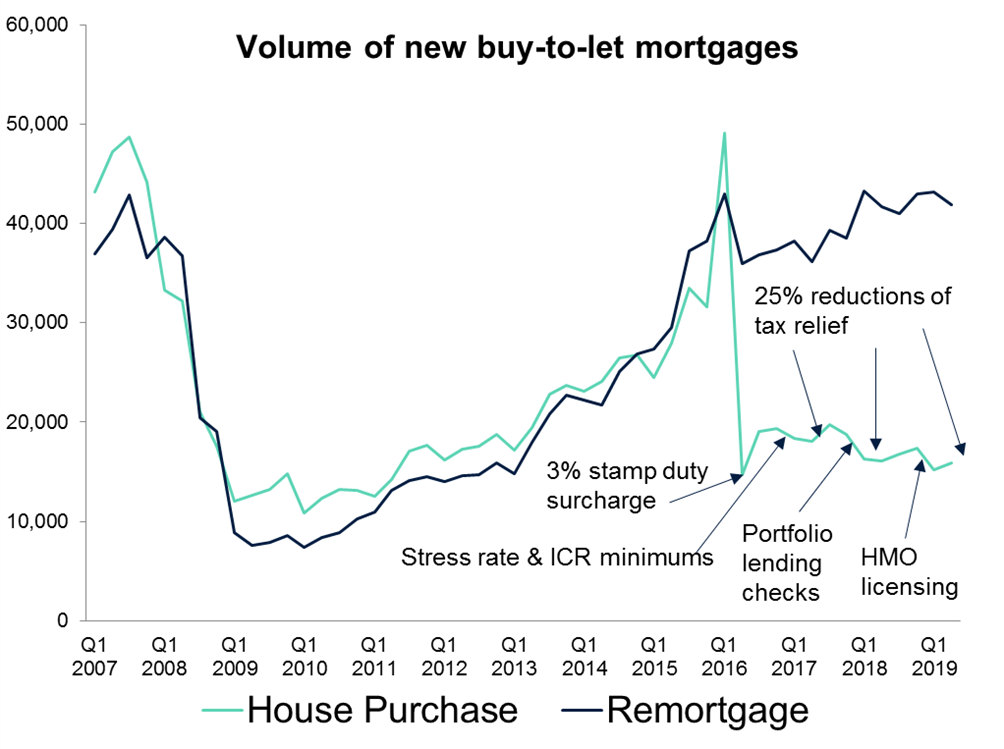

The changes in buy-to-let tax regulation announced in 2015 by the government implied that everyone buying a second home has to pay 3% additional stamp duty rate, which forced landlords to think twice before investing in a new project.

In 2017, the volume of BTL lending decreased to 12.5% — the lowest level since Q3 of 2013.

That very year, lots of homeowners resold their property, and real estate experts called on investors to turn to buy-to-let crowdfunding schemes.

Several reasons caused the boom on the UK BTL crowdfunding market:

- landlords got the opportunity to create property portfolios according to their preferences, interests and needs;

- BTL crowdfunding helps investors avoid higher taxes, such as the 3% stamp duty for deals no more than £40,000;

- crowdfunding platforms offer absolutely “hands-off” approach by hiring an agent who will be responsible for rental property management;

- some platforms offer discounts to angels who purchase several real estate units.

What does the UK BTL market look like now?

- As of June 2019, £234K BTL mortgages were transformed into home purchases ( £65K) and remortgages (£169K);

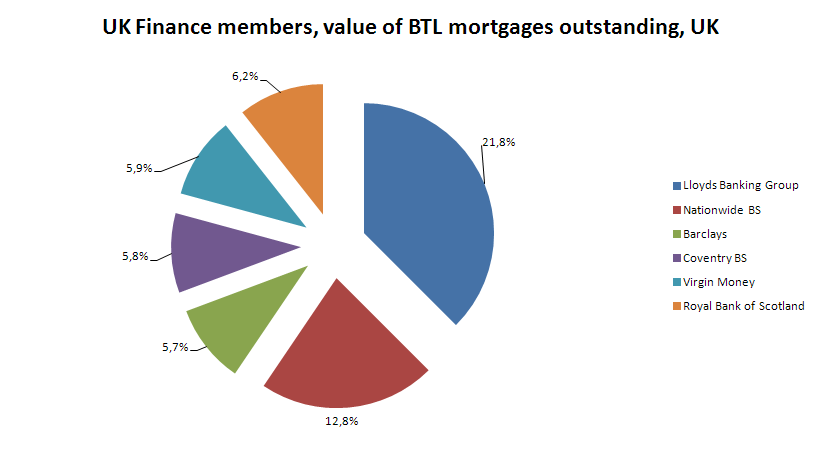

- Major BTL providers are Lloyds Banking Group, Nationwide BS, Barclays.

- In 2019 the total volume of BTL mortgages was £36B (home purchases — £8.7B, remortgages — £27.3B );

- Experts calculated that up to 4.5M Brits could occupy BTL properties;

- 64% of Brits are owner-occupiers (14.8M), 17% – live in social rented properties (4M) and 19% (4M) live in private rented property;

- cities producing the best net rental yields are Manchester, Salford, Portsmouth, Cardiff.

Types of BTL investments

Student BTL — properties (typically HMOs) built specifically for the young audience. They’re projected to bring higher rental yields and are cheaper comparing to other types.

Risks:

- student properties are typically occupied during the term time;

- students are usually short-term tenants with a limited credit history.

Residential BTL — rental homes and apartments for families. This type of investment is less risky since tenants have more stable status and income, which ensures the consistency of rental payments.

Types of BTL properties

- New buildings — expensive yet capable of attracting more roomers.

- Property under construction — property development cost tends to be lower than the market value since investors undergo considerable risks until the project is completed.

- Renovated buildings — require lots of efforts on estimation and project budget planning, yet projects of this kind can start generating income quicker than new and off-plan buildings.

Where to invest in buy-to-let crowdfunding

LandBay — a lending platform for specialist buy-to-let mortgages, providing an easy and flexible solution for brokers. Last year, LandBay has exited the retail peer-to-peer lending market to focus only on institutional funding for buy-to-let mortgages. At the moment, the company is refreshing its buy-to-let product range to extend its product offering to an even wider range of borrowers and landlords across the UK.

The House Crowd — a peer to peer lending platform offering property development investment and Innovative Finance ISA. The provider has good records: to date, The House Crowd backers have poured more than £120 million into real estate development.

Crowd With Us — another property crowdfunding portal from the UK matching backers with property deals. All the projects on Crowd With Us have huge potential to add value. Backers can start with £1,000 and then increase the investment amount to build a diversified portfolio. Appointed letting agents are responsible for managing properties funded via Crowd With Us for 10% fee.

Crowd2Let — a Newcastle-upon-Tyne-based company with a focus on residential buy-to-let property investment, refurbishment and management. The platform has already financed 750 investment properties with £40 million collected from individual investors and corporate organizations. Min investment amount is £500.

How does BTL crowdfunding process is set up?

- Provider receives applications from residential property developers and selects the projects which meet the platform requirements and have passed the due diligence check.

- Backers make investments until the project is fully funded. Some platform owners participate in property deals on a co-investing base sharing the risks with other backers.

- Crowdfunding provider establishes a dedicated company (Special Purpose Vehicle, or SPV) to purchase the property and create the ownership rights for investors who become shareholders in SPV.

- Assigned agents manage rental property and tenants for an established fee. The income generated by rental payments is split among shareholders according to their proportion of ownership.

Benefits of buy-to-let investments for platform owners and backers

Let’s start with angels. Why should they invest in the buy-to-let via crowdfunding platforms?

Accessibility

In a traditional pattern, buy-to-let mortgages are expensive: deposit, fees, and interest rates on them are much higher than on residential mortgages.

In addition, the property may be repossessed in case a landlord doesn’t make repayments on his/her mortgage. The success of the deal depends on the amount of money a landlord can deposit.

Crowdfunding makes BTL deals more accessible to ordinary people since platforms don’t require sufficient sums of money to be frozen on a deposit or paid as loan interest.

What’s more, you can still invest even if you can’t easily qualify for a mortgage

Less regulation and taxation

That very stamp duty we’ve mentioned earlier is to make buy-to-let even a large burden for landlords.

It adds up to the initial BTL investment and scares away the majority of potential homeowners.

In property crowdfunding, it’s an SPV who pays the additional 3% stamp duty land tax, which allows backers to avoid tough regulation and high tax burden. For instance, in Property Partner’s FAQs, they say that it’s possible to elect Stamp Duty Land Tax if buying more than 6 property units.

Diversification

BTL crowdfunding portals offer investment portfolios to reduce the risks of price volatility.

In the traditional pattern, it’s hard to predict whether rentals can cover the BTL mortgage repayments or the apartments will be occupied all the time.

Through investing in different properties located in different regions, angels can reduce this risk.

Delegating property management

Typically, landlords don’t consider the costs of letting rental apartments, property maintenance and management, unforeseen expenses and low seasons when choosing the traditional buy-2-let.

Crowdfunding platforms take into account all the risks of a buy-to-let investment in property crowdfunding and offer net returns.

In addition to unexpected costs, property management and liaising with tenants require lots of efforts, which are, though minimized if you invest via a platform.

Exit strategy

Property assets are great, but they’re very illiquid.

When it comes to turning a rental block into cash, you may experience difficulties. With secondary markets built-in crowdfunding sites, it’s way easier – landlords receive capital gain when reselling their ownership rights to other angels on secondary markets. However, only some companies provide investors with this opportunity.

Perks for platform owners

- Appealing prospects of the industry;

- various niches to occupy;

- expanding the pool of investors.

Wider client base

Almost everyone with idle cash and desire to become a landlord can register on the platform.

Shojin, for instance, considers everyone aged at least 18 and based in the UK with a National Insurance number as a potential client.

Homegrown has the same requirements and accept members who are over the age of 18 and not a resident of the USA, or any of the countries listed on the OFAC Sanctions List.

During the registration, fundraiser conducts KYC/AML checks and accepts/rejects an application.

Co-investors

For companies like Shojin, buy-2-let are a good chance to attract more co-investors with similar interests and perspectives.

The platform carefully vets each project and select only those developers who are reliable and projected to deliver profits. This generates trust and forces clients to take part in BTL deals.

More clients, more revenue

The fees structure varies from a company to company.

Homegrown charges 5% for deal origination and 15% of profit share.

Shojin doesn’t ask for any administration fees; to cover transactional costs, they charge 2% of an investor’s funds poured into the project.

Property Partners have recently introduced the AUM (assets under management) fee ( 1.2% per annum on portfolios valued up to £25,000 and 0.7% on those valued over £25,000) plus to an account fee (£1.00 per month + VAT). In addition, they have a 2% transaction fee, and 3.0% + VAT – sourcing fee.

Property crowdfunding platforms with a buy-to-let model

Some of our clients have already experienced the benefits of buy-to-let opportunities and added this option to their product portfolio.

Shojin

It’s a high-tech crowdfunding company operating in the institutional-grade real estate domain. Shojin is a partner to each and every angel on their platform as they have a co-investing operational model at their core.

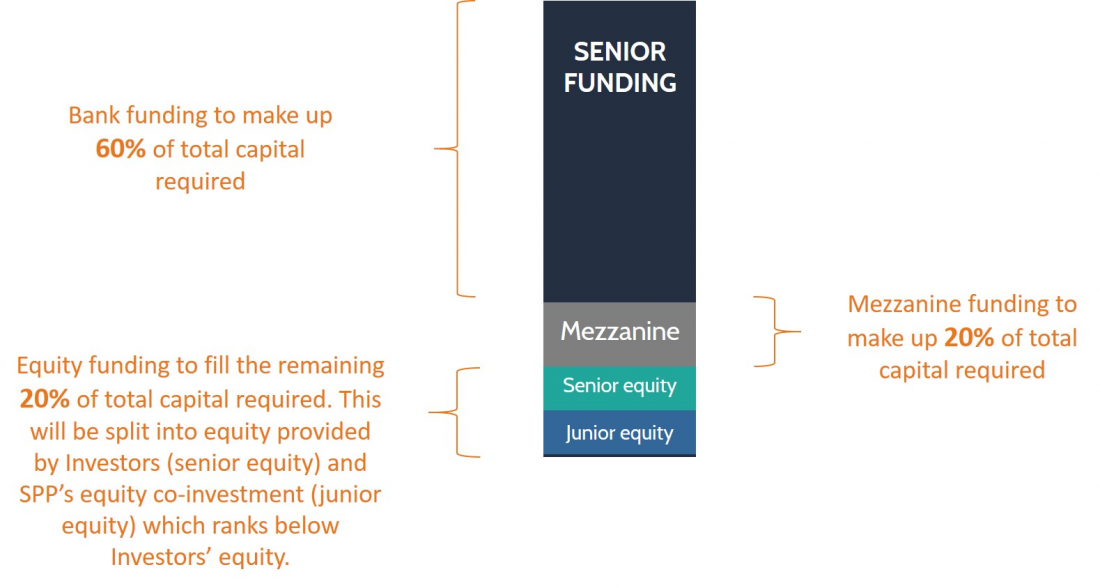

Shojin knows that many buy-to-let investors are turning to crowdfunding. That’s why it created a very sophisticated product — mezzanine fundings. The point is that investors are divided into two large groups:

- backers who pay taxes at higher rates and concentrate more on the capital gains;

- lower-tax payers who rely on income.

Mezzanine funding has 4 layers.

- 1 layer (60% of total capital) is funded by a bank on a fixed interest rate

- 2 layer (mezzanine funding) covers 20% of total capital and is provided by lower-tax investors who can earn an annual fixed rate of 5%.

- 3 layer is supported by equity investors who are more interested in capital growth. Equity investors can resell their shares on the secondary market and take advantage of the tax allowance.

- 4 layer – junior equity co-investors.

Shojin has revolutionized BTL deals by making them more accessible and appealing to all kinds of investors.

Learn more about Shojin project in our blog.

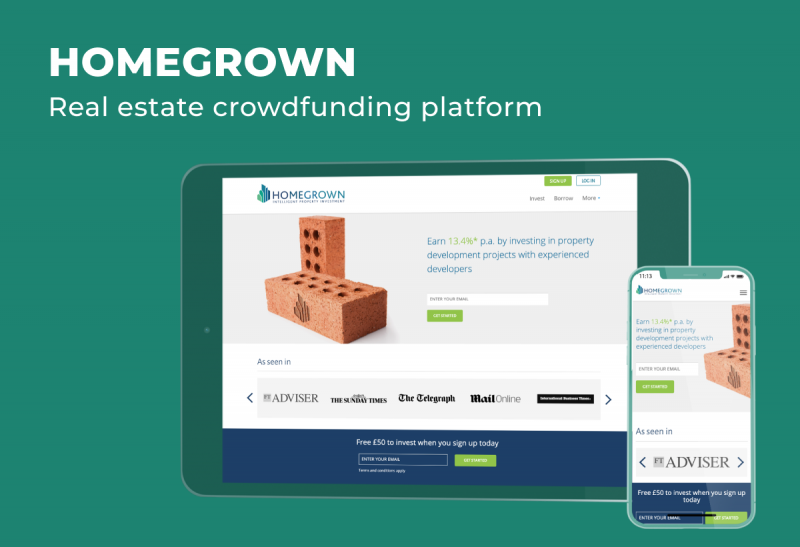

Homegrown

If an investor is looking for an option to invest in high-quality residential development projects alongside professional angels, Homegrown is a great option for that.

Backers can build custom diversified investment portfolios by donating £500 as a minimum.

An average projected return is 13,4% and is normally received in 18-36 months.

Every project undergoes thorough checks by independent platform experts; 90% of applications are rejected since they don’t meet the provider’s criteria.

Buy-to-let deals at Homegrown work this way:

- A backer chooses a property and invests in a development project.

- Once the total sum is collected, Homegrown establishes a UK limited company.

- The pool of investors become shareholders in the SPV and continue monitoring the performance of portfolio via their dashboards.

- The platform organizes shareholder voting on key decisions that impact the SPV

- Profit and share returns are generated between investors and the developer.

Wrapping up

The practice of buying a property in the UK to “let it” is being reborn and rediscovered by online crowdfunding fundraisers.

The buy-to-let domain has been shifted to the digital realm and now is open to everyone. Generation X consider BTL property projects as an additional income to their pension schemes. Millennials are also taking an interest in real estate crowdfunding with its hands-off approach.

Fundraisers welcome new landlords and share rental income on a co-investing basis.

We can safely say that the new mainstream is here to stay, so now it’s the right time to join the party and equip your crowdfunding platform with the new option — buy-2-let investments.