The Fintech Revolution is not a fairy tale or science fiction; it’s reality changing the shape of the global financial system.

P2P loans at a fingertip, conscious crowd investing, cryptocurrency payments, automated financial advisors — these things have appeared thanks to the close collaboration of FinTech startups and traditional institutions.

While the former get funding for their out-of-the-box projects, the latter take advantage of digitisation. Undoubtedly, the results of this alliance are beneficial for both parties.

But what if the FinTech industry continues developing at breakneck speed? Does it mean the end of traditional banking?

In today’s article, we’ve tried to find the answers.

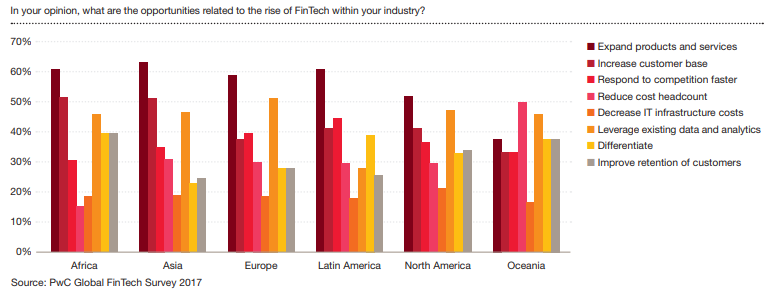

The current state of the FinTech industry

Let’s start with a few facts about the state of the market before we dug deep into how FinTech driving financial services innovation.

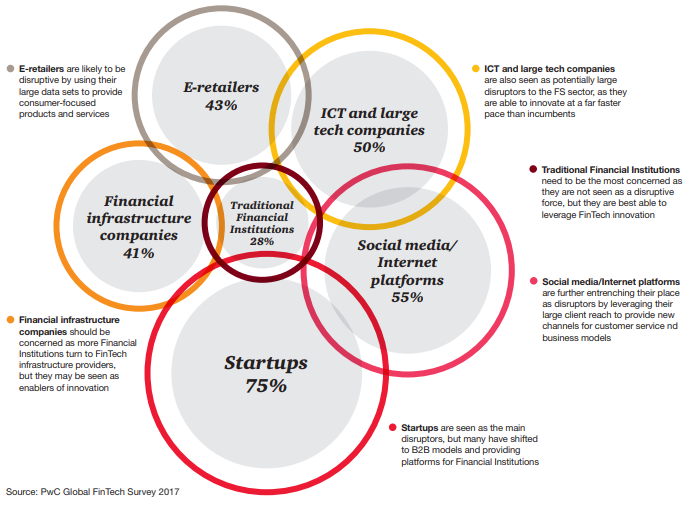

Fact #1. Traditional financial institutions are believed to be one of the most likely entities to undergo disruptive changes in the next few years.

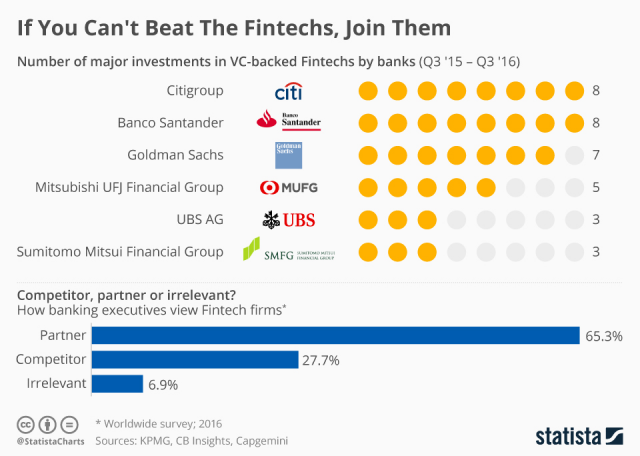

Fact #2. The largest investors supporting FinTech startups are financial institutions: Citigroup, Banco Santander, and Goldman Sachs, which proves their interest in the evolving field.

In the US, for instance, FinTech firms gained 63% of total investments poured into the financial industry.

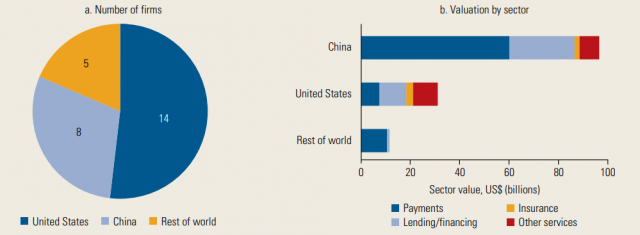

Fact #3. The majority of FinTech “Unicorns—startups with a valuation of over $1 billion—are based in China and the US.

Before the lockdown, the FinTech industry was evolving at a breakneck speed, but COVID-19 has adjusted its development path.

According to CBInsights, Q1’20 was one of the worst quarters in 2 years for FinTechs backed by venture capital firms.

Only 3 new unicorns joined the market. To compare, in Q1’19 there were 8 emergences.

New entrants:

- Pine Labs ($1.6B valuation) — a new-age merchant platform to accept multiple modes of payments.

- HighRadius ($1B) is a SaaS platform for companies that leverage artificial intelligence-based autonomous systems

- Flywire ($1B), allows organizations to optimize the payment flows while eliminating operational challenges.

During hard times, people tend to avoid risks and deal only with solid trustworthy financial institutions.

But cred.ai, a Philadelphia-based fintech start-up, has proved otherwise. This unicorn raised over $18m in Series A funding. Positioning itself as a bank’s alternative, cred.ai offers a solid metal credit card with no fees, no interest, credit optimization, self-destructing account numbers and other perks.

Its target market is Millennials and Gen Z.

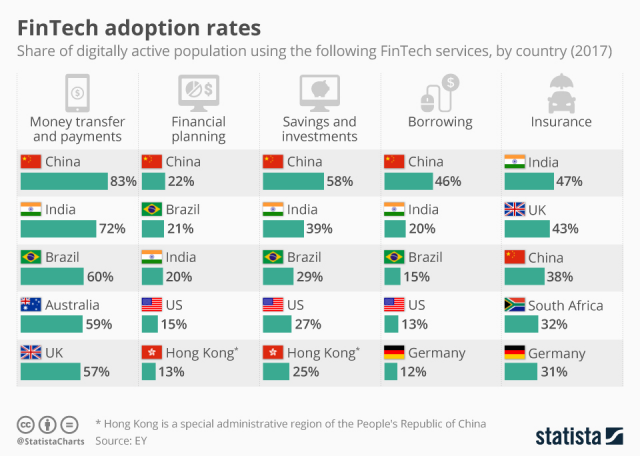

Fact #4. The most used features in financial application development all over the globe are:

- money transfers and payments;

- savings and investments;

- borrowing;

- financial planning;

- insurance.

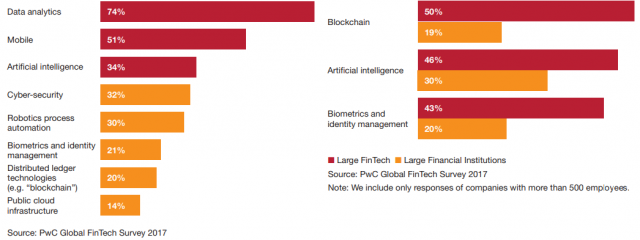

Fact #5. The preferable technologies for the financial business are Data Analytics, mobile development, Artificial Intelligence, and Blockchain.

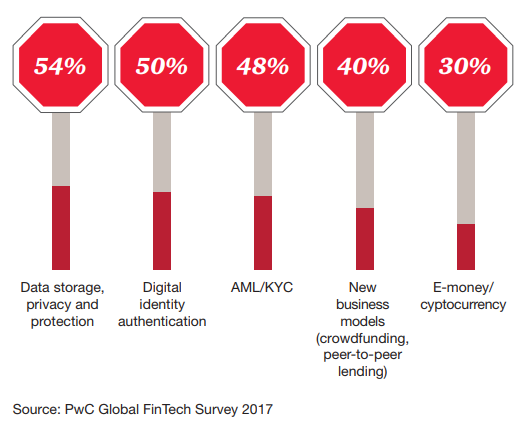

Fact #6. Areas that lack legislative coverage are Data storage, Digital authentification, AML/KYC, crowdfunding, and cryptocurrency.

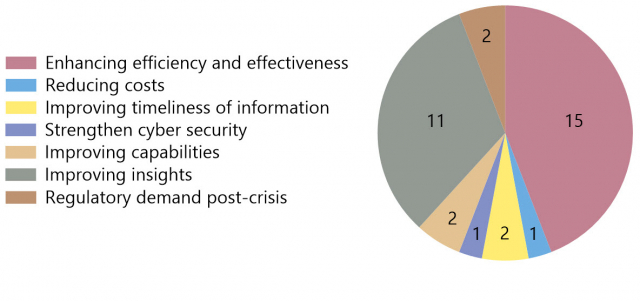

Breaking down the impact of FinTech on financial services

Originally FinTech startups and traditional banks were rivals fighting for every client, but now everything has changed because of the FinTech disruption of financial services.

Better client service, enhanced financial security, more opportunities for individuals and businesses, and many more other things are the fruits of the creators and incumbents’ partnership.

So how did this become possible?

Big Data and risk assessment

All the personal records kept in gadget storage refer to Big Data and if applied appropriately can reveal behavioural patterns of existing and potential clients.

AI and ML algorithms deployment helps FinTechs and investment firms build strategies aimed at a more personalized portfolio, superb client service, and less risky transactions.

What is more, advanced technologies can be used for fraud detection by identifying unusual user activity based on behavioural patterns.

Fintechs have recently started experimenting with Big Data for compliance purposes. They’re developing tools and solutions which help incumbents meet the established requirements.

Security and client experience

Another example of the impact of FinTech on banks is positive changes in private data protection and customer experience.

Several data breaches that occurred in different parts of the world not so long ago have forced incumbents and their younger partners to take notice.

This summer the scandal with Wirecard rattled the FinTech world. One of the largest payment providers failed to meet the mandatory audit by disclosing a $2.1b hole in its accounts and admitting a sophisticated global fraud.

For the rest of the players, this case provided several lessons:

- the market players understand the importance of creating a “compliance culture” (a set of rules and standards) they are to follow early;

- streamlined expansion implies that FinTechs compare the growth prospects and compliance capabilities;

- AML/KYC checks are integral elements of the internal structures of FinTechs enabling companies to vet and monitor clients.

Georg Hauer, a general manager of Klarna, one of the most highly valued European fintechs, believes that gaining trust should become the highest priority for FinTechs who need to make sure that their technology works seamlessly, always act in the consumer’s best interest and cater for their needs at any time.

But the above-mentioned scandal wasn’t the last in the row of fraudulent cases.

Not so long ago, ING subsidiary Payvision, a payments processing provider, was accused of facilitating fraudulent transactions worth €131.2m. 289 European consumers lost their money over a four-year period, from 2015 to January 2019.

Payvision is called The “Netherlands Wirecard” and blamed for “helping scammers in big style fraud”.

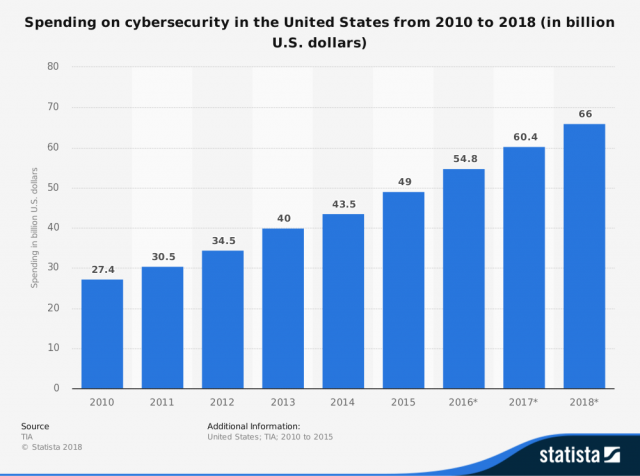

As FinTechs mostly rely on mobile applications for banking and financial services, the risks of unauthorised access to personal financial records, accounts, and digital wallets have increased over time.

Better cybersecurity and, hence, customer experience can be achieved by strengthening the infrastructure of applications and the usage of firewalls.

Cloud services require special measures and techniques for detecting automated attacks, protecting each kind of service separately, and developing a robust architecture.

Personalised automatic support

We started by saying that it’s the demand for personalised financial services that drive incumbents and startups to join their efforts.

So, how does FinTech affect banks’ customer support?

Clients make several demands to the bank support: communication should be convenient, assistance – relevant to their particular situation and the feedback – instant.

To meet these requirements, incumbents deploy various channels – messengers, chats, help centres.

This omnichannel approach also works great for promoting new products and collecting clients’ data.

What’s more, some banks deploy the co-browsing technique that allows the support specialist to assist as if they’re sitting next to the customer and pointing at the monitor.

It’s a great go-to for online procedures such as loan formalisation, opening a bank account or insurance arrangement.

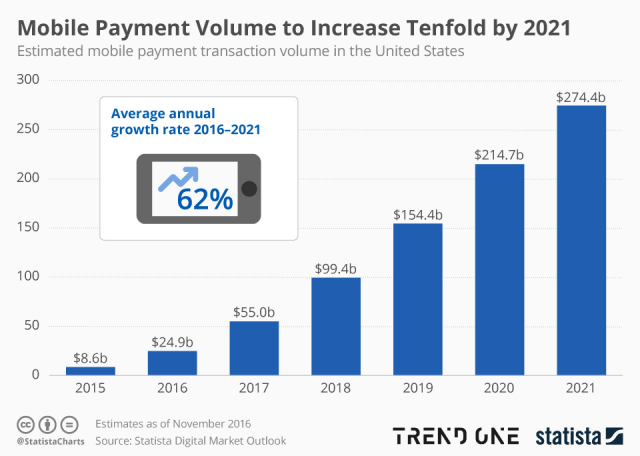

Total digitalisation in transactions

The next point in our “How FinTech impacts banks” chart is progress in transaction banking.

Even though every transaction is now accessible 24/7, there are still a good number of customers who prefer traditional methods for paying utility bills, making money transfers, or repaying loans.

Innovations in digital transactions are going to attract even the most conservative clients.

The first trend that deserves special attention is omnichannel banking enabling users to make transactions in every environment – web platforms, applications, social networks.

Other positive changes refer to decreased transactional fees, better transparency, and lower error risk, which has been achieved thanks to blockchain deployment.

Products and services of the new generation

Having embraced the sense of innovation, banks are now competing for the most sophisticated products or services.

Below you will find the best practices of how FinTech is disrupting banking services.

- Digital-only banks function without physical branches delivering solutions online. Among the best-known neo-banks are N26, Penta, and Chime.

- Joint current accounts such as Monzo deal with various currencies, card types, and user categories allowing clients to track their expenditures and manage savings.

- Voice and face recognition techniques are applied for providing access to users’ accounts. Atom Bank is one of the institutions deploying these methods.

- AR/VR gives a chance to financial entities to gain an advantage over competitors. For instance, the Commonwealth Bank of Australia has already developed an app delivering an immersive experience for real estate buyers and sellers.

The global crisis forced FinTechs to innovate even more. The players invent new ways of providing relief for their clients (decreased fees and chargebacks) and create new forms of collaboration.

For example, Kabbage in the partnership with Lendio, Finix, and Fundera launched a platform where consumers can buy gift certificates to support local small businesses during the coronavirus crisis.

Another example is Revolut and its charitable-giving feature for users who want to support those affected by COVID-19.

The current market environment is evolving rapidly and in order not to leave behind, FinTechs are introducing new products:

- Trade Ledger, Wiserfunding, Nimbla, and NorthRow have joined forces to build a turnkey origination and underwriting platform for lenders of all types to offer funds to businesses;

- Innovesta from Israel has developed COVID-19 Resilience Innodex (CRI) calculating the risk score and ability of businesses to withstand the effects of a pandemic;

Iwoca provided clients with new lending capabilities through the OpenLending platform.

Great shifts in human resources

FinTech is not only modifying the business models and infrastructure of high-street banks, but it also triggers considerable shifts in their human resources.

New FinTech departments created in banks raise the demand for specialists with skills and expertise in both finance and development.

As a result, a lot of innovative positions for cybersecurity analysts, product managers, compliance experts, and data specialists have flooded the labour market.

On the one hand, it stimulates the younger generation to pick a career path that will be relevant in the upcoming years.

On the other hand, it forces companies to put efforts into training the existing staff, arranging educational events, and improving the tech expertise of human resources.

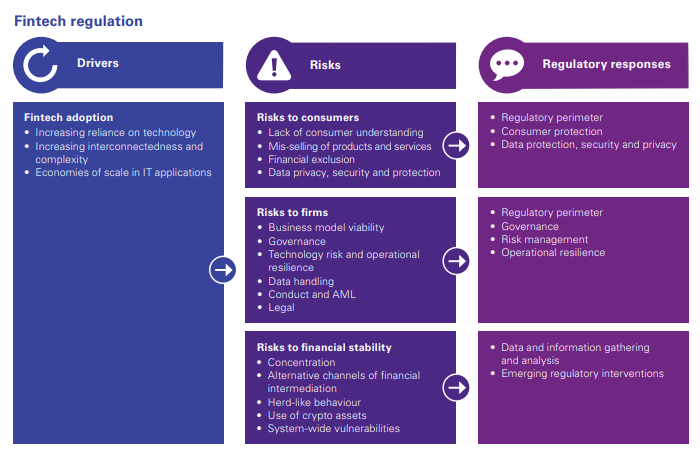

How does FinTech affect the financial system? Risks and challenges

It wouldn’t be fair if we concealed the flip side of the FinTech startups and banks’ collaboration.

The fast implementation of cutting-edge technologies raises challenges for financial firms and the whole industry.

Risks to firms:

- some business models can’t stand the new competition and turn out to be unsustainable;

- the official requirements for financial organisations may be ambiguous, vague or unrealistic;

- the widespread use of technologies may lead to serious risks in operational activity;

- banks operating globally may face challenges related to the differences in regulatory frameworks of different countries.

Fintech impact on financial services and market stability:

- leading FinTech providers and successful alliances between startups and incumbents are becoming systemically important;

- the current legislative base doesn’t cover all the issues related to the activity of non-bank institutions;

- the use of cryptocurrencies may cause price volatilities and affects payment systems.

Effects of fintech on the banking industry: new laws and regulations

The majority of the above risks can be eliminated by advances in the current system regulating financial markets.

Recently, regulating bodies in the UK, EU, USA, and other countries have taken their first steps in this direction.

The PSD2 directive issued by the European Commission is aimed at making global payments more secure, protecting data on personal accounts, and entitling banks to use the services of third-party providers.

The SEC and the Consumer Financial Protection Bureau have expanded the network of their offices to help FinTech organisations in different states to meet the industry requirements.

The Office of the Comptroller of the Currency offered a special charter to help FinTech firms in making money cross-border transfers, arranging loans and enlarging their network.

Besides, the FED has facilitated the process of banks and financial firms M&As.

The Mexican “Fintech Law adopted in 2018 has created a solid ground for applying financial technologies in the bank industry and enhanced healthy competition on the market.

The impact on the future of banking: what experts predict

Obviously, the FinTech industry doesn’t intend to slow down and will only continue surprising with brand-new models of collaborations between young startups and established banks.

If you’re in this topic, you need to know the influence of FinTech on the finance industry in years to come.

So how will FinTech affect banks in the nearest future? There are several aspects of this influence.

Openness and collaboration. The financial revolution is based on open innovation bringing together incumbents and third-party providers. Smart regulation will ease sharing of data, knowledge and ideas between market players.

Accessibility and financial support. New laws and rules will help financial firms easily enter the market and high street banks — to implement the FinTech aspects in their business models efficiently. Through fundraising and venture investing channels, organisations will be able to collect the necessary funds in a matter of time.

Trend #1. Open Banking will offer more choices for bank clients.

The new concept was initially offered in the UK and then spread to the rest of European countries.

The initiative implies that banks will partner with third-party companies by handing over users’ data to the latter via application programming interfaces.

It is expected that open banking practice will boost competition, drive innovations, and deliver a better users experience.

Although digital-only banks were equipped and prepared for the lockdown, they have suffered a lot from the global crisis. Being additional secondary means for specific financial purposes, now they see a downward trend in daily service banking usage.

Fincog has developed the Fincog Challenger Bank Index and analysed the performance of neo-banks across the globe. Here are a few of their findings:

- trading services continue to be the most stable and keep attracting investments;

- daily banking and foreign currency neobanks have felt the negative impact of the coronavirus;

- digital challenges show good resistance to challenges;

- consumer lending has declined while business loans are on the rise.

The experts from the Financial IT believe that one of the lasting effects of COVID-19 will be loans and similar products’ delivery through Open Banking.

The point is that neobanks find the current environment very challenging and to be competitive they have to serve the current needs of businesses and households experiencing financial stress.

Trend #2. Small banks are willing to jump on the bandwagon of FinTech.

In the aftermath of the financial crisis, lots of local banks were left behind the rest of the competition.

And it’s high time they took action to revive and found their place in the sun.

Several US banks, Evolve Bank & Trust, Cross River, and Sutton Bank, have established strong relationships with startups.

While young companies reach out to their client base and gain regulatory protection, incumbents conquer the mobile banking app market.

Trend #3. Traditional lending will become faster and more accessible.

The underserved categories of bank clients can breathe a sigh of relief as the lending process is going to become less painful and time-consuming.

The FinTechs and incumbents tandem is working hard on enhancing current credit score assessment patterns and risk management systems, which will lead to faster decision-making.

Trend #4. Regulatory Technology is to eliminate compliance efforts.

The RegTech is already here to improve current regulatory flows with the help of advanced technologies, Big Data analytics, and cloud computing in particular.

The RegTech is to help financial institutions easily and painlessly adapt to ever-changing law systems.

SupTech (Supervisory Regulatory) may become another mainstream greatly benefiting the financial stability of FinTechs and incumbents.

A month ago, The Financial Stability Board (FSB) published a report on the use of supervisory (SupTech) and regulatory (RegTech) technology by FSB members and regulated institutions.

The document explains the opportunities offered by SupTech and RegTech related to data collection, analysis and storage.

Regulatory bodies get a tool to improve analytical capabilities and supervision policies. Regulated companies are able to enhance risk management systems, improve decision-making processes, and facilitate compliance procedures.

This trend especially concerns compliance issues, transactions tracking, trading, and reporting systems.

As FSB states, the majority of respondents have already established the SupTech system since 2016, which significantly increases their chances of solving compliance issues and building trust.

Trend #5. Banking as a Platform (BaaP) continues gaining momentum.

Platform-Based banking is evolving by leaps and bounds, gradually replacing the traditional product-centred approach and vertical business models.

The idea is to allow third-party providers to develop banking solutions having full access to the inside information of incumbents.

In this sense, BaaP resonates with the Open Banking concept as both are intended for yielding benefits to all parties – FinTechs, clients, and banks.

These were only a few movements we’re going to observe in the nearest future. FinTech has an enormous potential that will be unleashed very soon.

Our FinTech projects

Our main focus in FinTech is mainly on online investment and crowdfunding solutions for various niches, market sectors, and business models.

While we have built many FinTech platforms for our clients, there is also LenderKit — a stand-alone FinTech solution that we created based on our experience.

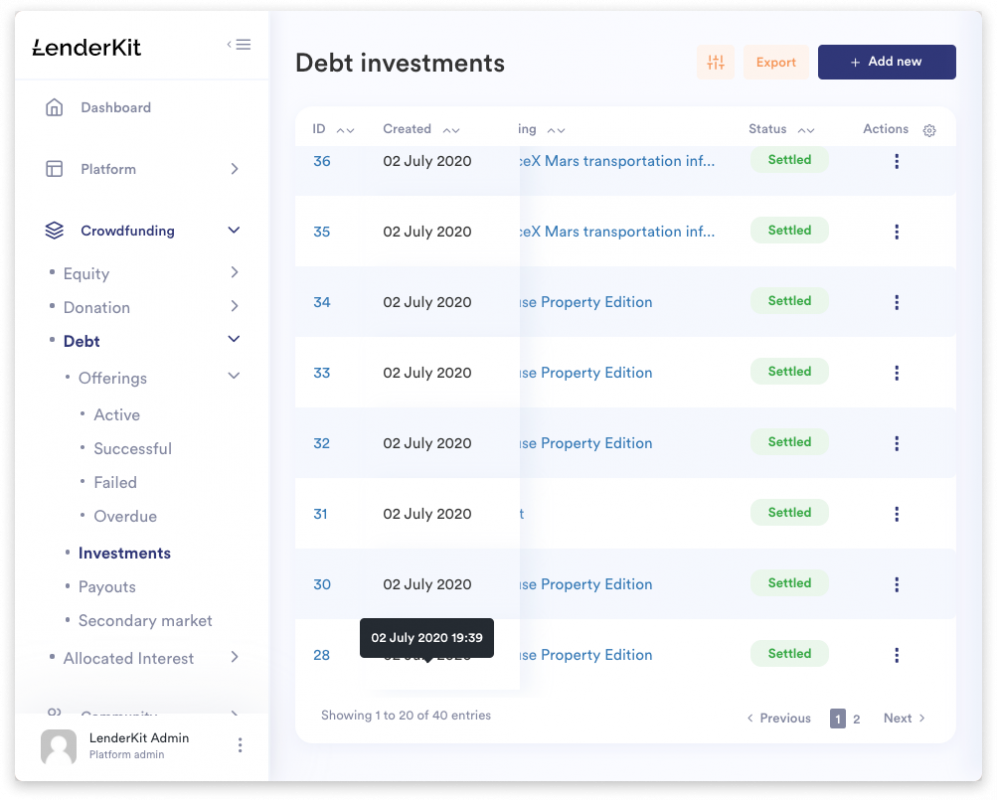

LenderKit

LenderKit is a crowdfunding and online investment software for businesses that are going to enter the market of alternative financing.

It can be used for real estate investing portals, and P2P lending platforms with debt or equity investment models.

LenderKit comes in a bundle with essentials like a powerful back-office, automated KYC/AML procedures, the built-in CMS and a secondary market.

InvestMySchool

InvestMySchool is a UK-based fundraising platform that helps independent schools and educational organisations.

It deals with loans and donations, enabling parents, relatives, and alumni back appealing projects that aim to improve education and facilities.

What sets the platform apart from the rest is that fundraisers can amend loan aspects themselves: length, interest rate, repayment scheme.

Besides, InvestMySchool offers lower fees than other similar platforms.

In closing

Certainly, a complete transformation of solid brick-and-mortar banks into digitised service providers won’t happen in a blink of an eye.

It requires a lot of time, resources, and effort.

However, the mainstream we can observe right now promises to drive more customer-focused rather than product-oriented banking solutions.

The synergy generated by the FinTechs and incumbents partnership is to benefit all the stakeholders.

For FinTechs, there will be fewer entry barriers, for banks—more opportunities to satisfy all the generations from X to Z, for us—no need to choose between alternative service providers and mature banks.