Everyone knows Bill Gates as the richest man and the founder of one of the most successful tech companies in the world.

But he’s also the most generous philanthropist and the leader of Bill & Melinda Gates Foundation whose main task is to combat extreme poverty and poor health in developing countries.

Interoperability of mobile money (MMI) is one of the aspects the Foundation focuses on.

In simple terms, MMI means that if you have some money topped up in your Vodafone account, you can freely transfer it to your friend using another Keepgo.

Bill and Melinda believe that tech innovations and new approaches will help people and SMMEs improve the entire standard of living and boost the economy.

Let’s learn how.

What’s the impact of mobile money on emerging markets?

In a broad sense, interoperability is the ability of two or more systems to exchange information in a pre-defined manner, just like Facebook can interact with Apple iTunes or Google Play Music, for example.

MMI covers the retail banking and mobile payments where interactions take place between any service company (bank, mobile operator), through any medium (smartphone, PC) and in the form of any product, mainly as payments and money withdrawals.

According to NextBillion, there are several types of MMI:

- account-to-account interoperability (A2A). For instance, three users of different network providers in Kenya (Safaricom, Airtel and Telkom Kenya) can send money to each other through the ecosystem in real-time;

- agent interoperability takes place in off-net transactions. A payer, a client of Agent A, sends the money to a payee, a client of Agent B, who wants to cash out. The payee is sent a code via an SMS, which he/she needs to show to the payer’s mobile money service to get the remittance in cash;

- ecosystem interoperability relates to operations between financial institutions such as banks, payment systems and mobile money operators and takes the form of merchant/ payments.

Also, there is domestic interoperability when you can send money between different mobile networks in one country. If you’re in Tanzania and making a transfer to a friend in Nigeria via Western Union, it’s what they call International remittance or International money transfer (IMT).

Despite being here for over a decade, only the last year mobile money products in emerging markets were taken to a new level.

What happened in 2019?

- the number of registered accounts reached 1B, and daily transactions grew to 2B. It means that one in eight people engages in mobile payments daily;

- in June 2019 alone, at least 26 million unique customers made savings via mobile money (it’s 39% higher than in 2018);

- 60% of service providers reported a positive EBITDA, which means that revenues generated by mobile money were directed into advanced products and services, network expansion, and reasonable agent commissions

- the number of agents has tripled over the past five years and in rural areas agents have a transformative impact on financial inclusion;

- and what’s very important, is now the ratio of digital to cash-based transactions is 50% higher than it was in 2017.

These are just numbers.

But what’s behind them is a leapfrog towards overall financial inclusion and fewer unbanked people.

GSMA, one of our clients, who is very much involved in the adoption of mobile money in emerging economies, regularly conducts surveys on the state of the industry.

In a recent survey, they highlight a few significant trends changing the industry landscape:

- service providers are becoming commercially sustainable;

- ‘payments as a platform’ model is gaining momentum;

- new customer segments, including traditionally underserved and cash reliant customers;

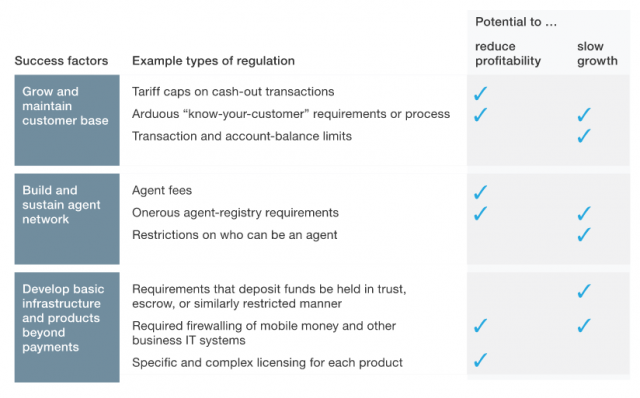

- new regulations (sector-specific taxation and data localization requirements);

- mobile money driving financial inclusion for women;

- unlocking access to utility services;

- digitization of agricultural value chain payments.

MMI in times of the COVID-19 pandemic

In March, GSMA issued a report with the industry snapshot during the global lockdown. Earlier, we wrote that MMI has a great potential to solve global economic and social problems. The insights from the GSMA survey prove this.

Last year, the number of registered mobile accounts grew by 12.7%, which exceeded the projected growth rate. This boost in mobile payments was caused by the global shift to a cashless society, relaxed onboarding requirements for new players, and more flexible KYC procedures.

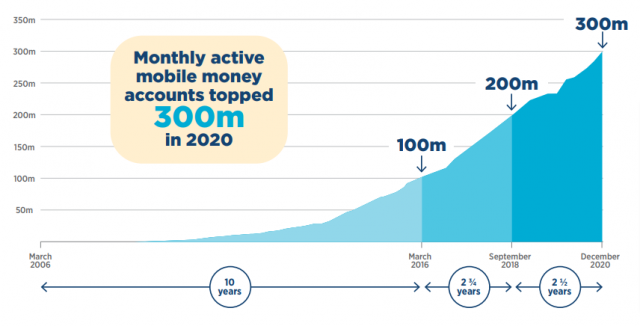

Another important indicator, the number of monthly active accounts, has reached an important milestone of 300M accounts. To compare, in 2018 there were 200M regular MMI users.

Now, people tend to use mobile payments for more advanced transactions like merchant payments, international remittances, and bulk reimbursements.

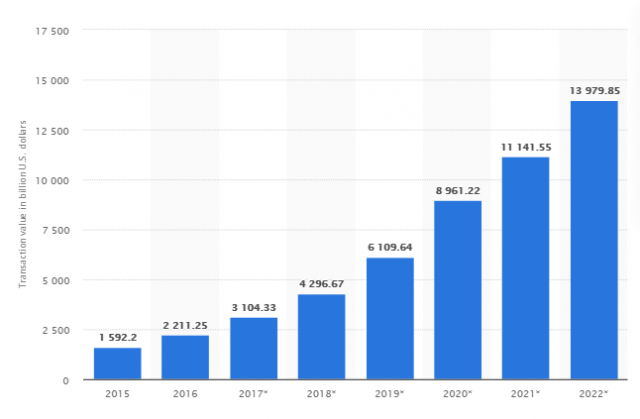

With the increase of registered and monthly actives accounts, the total transaction volumes have more than doubled since 2017.

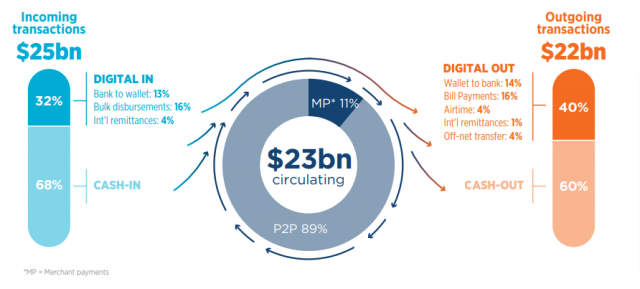

Cash-in and cash-out remained the most popular mobile transactions.

The ever-rising demand for MMI services has forced players to develop mobile money APIs and establish business relations with partners and third parties.

The GSMA has created a Mobile Money API Compliance Verification Service for such use cases: agent services, bill payments, account linking, merchant payments, bulk disbursements, international transfers, P2P transfers, and recurring payments.

Benefits and challenges of mobile money impact

There are plenty of characteristics of developing countries, including:

- low per capita real income, e.i. the population doesn’t earn enough money to invest or save money;

- high rates of unemployment;

- the domination of the primary sector (75% of the population is low-income);

- low financial literacy and education level;

- a large amount of cash in circulation and a significant number of unbanked people.

The further expansion of MMI is going to solve the above problems partially. From successful business cases, the benefits of mobile money interoperability become apparent:

1. The more info, the better decisions

Currently, there’s only 33% of the world’s adult population with credit history records. Often, lenders lack info and reject loan applications. The partnership between mobile providers and credit bureaus is going to provide more data for more informed decisions.

2. Save. Plan. Prosper

Savings and investments are the essential products offered within the MMI system. Having access to smart investments opportunities, people will be able to cover such needs as education, home improvement and health support. Plus, they’ll have a financial cushion in the event of seasonal loss of employment.

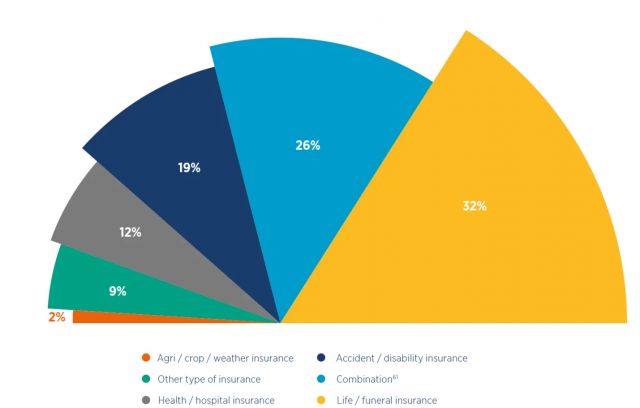

3. Inclusive insurance

The majority of the population in emerging companies is vulnerable, and mobile insurance is going to solve this problem. According to GSMA, over 14M of new policies were issued in 2019 alone, the most popular of which was life, health and accident insurance. Again based on Big Data coming from mobile devices and apps and providing patterns of typical behaviour, providers can offer more relevant products to different types of clients.

4. Saying no to the gender gap

Gender equality is one of the burning issues in the developing world. Women are consistently less aware of mobile money than men and often don’t own any mobile account. The main reason for it is a preference for using cash. Another one is low literacy, and digital and financial skills. New products within the MMI framework are to better target existing and potential female customers.

Other merits include: expanding the reach of utility services, providing humanitarian cash assistance, making agricultural value chains more efficient

The success of mobile money in emerging markets: from Nigeria to Peru

Innovations continue to push boundaries in Sun-Sahara Africa, East Asia and the Pacific. We’ve collected the most successful examples of mobile money and financial services in emerging economies. Let’s see how little things can make great changes.

Nigerian-based Interswitch is an integrated digital payments and commerce company facilitating the electronic circulation of money between individuals and organizations.

The company offers solutions for individuals (Verve rewards and payment platforms), businesses (retail payments and funds disbursement), and opportunities for industries.

Interswitch’s financial inclusion system is based on agents who deliver services on behalf of the provider. These services include bill payments, cash deposits and withdrawals, among others.

A Ugandan startup Ensibuuko which is partially funded by the GSMA Ecosystem Accelerator programme strives to address the challenges around financial inclusion in Africa.

Microfinance solutions the company offers help businesses automate business flows like data, processing and payments.

Mobile Money & SMS Integration is a free add-on for any of Ensibuuko Microfinance software allowing clients to receive and pay-out funds and manage Telecom payment accounts.

In Ghana, Bank of Ghana launched the first MMI System aimed at making transfers across the various mobile money networks in the country smooth and comfy.

Citizens can quickly get access to the system. They should simply dial their existing mobile money shortcode to access the service, and the mobile network will provide the menus to use the MMI service.

The MMI system isn’t only limited to A2A payments, you can transfer money between banks accounts, mobile money wallets and e-zwich cards.

The objectives of the project are to reduce financial exclusion, lower the cost of transactions, increase service reach and reduce reliance on cash for payments.

Peruvian Modelo Bim mobile money platform is a collaboration between financial institutions, telecom companies, and the government. It’s designed specifically to better serve the nation’s unbanked and underbanked population.

The platform is innovative because it consists of three layers – government, telecoms, and financial institutions. Core operations users of Bim (“Bimers”) can complete:

- cash in/cash out;

- P2P transfers;

- P2B and P2G payments;

- specific services like airtime purchases.

Despite the challenges preventing the project from widespread usage, it will likely remain a great alternative to traditional banking services in Peru.

As a response to COVID-19, in Paraguay, the government has launched a subsidy programme, Pytyvõ.

Within this program, previously self-employed people and SMEs that suffered from the coronavirus impact received governmental disbursements.

Third-party mobile money providers involved in the project are Claro, Personal, Tigo, and Zimple.

Throughout 2020, the Paraguayan Government disbursed $289M to over 2M beneficiaries through Pytyvõ.

Solutions like Pytyvõ leverage MMI to facilitate financial inclusion, combat poverty in emerging economies, and provide government help.

Nano-credit loans offered by Orange Bank Africa are a good example of MMI addressing funding issues.

Orange Bank Africa offers two prime products: Tik Tak Loan and Tik Tak Savings integrated into both the Orange Money app and USSD menu.

The min amount customers can borrow is $9, with an average value of $44. As of 2020, Orange Bank Africa disbursed over 467K loans and let 61K customers open accounts via the app.

The solution benefits both parties: the bank gets extra data about clients who share their personal info when applying for a loan; customers — receive a loan fast and easy.

GSMA interoperability test platform

Reliability is the core feature of any MMI system. Since every developing country has a purpose of developing a robust ecosystem, there should be tools to test and support it.

GSMA’s Inclusive Tech Lab is currently developing the first joint test environment based on GSMA Mobile Money API and Mojaloop. Once the project is completed, it will enable digital finance service providers to test their systems across different use cases.

How does the system work?

Users select a scenario (e.g. service provider user testing), then choose a use case (e.g. account verification) and run reliability testing.

The platform solves complex testing scenarios through the simulation of the different ecosystem entities, the different APIs and different use cases.”

— Bart-Jan Pors, Director, Inclusive Fintech, GSMA

What’s under the hood of the Test Platform?

- user dashboard to track the day-to-day evaluation;

- minimal requirements for configuration;

- pre-built test cases;

- full-flow diagrams;

- automatic validation of messages.

Initially, the platform wasn’t designed to serve the needs of hub operators, but recently this issue has been fixed.

There were 3 issues the new release of the platform has addressed:

- correctness (new participants have to follow the correct processes according to the interoperability protocol);

- connectivity that should be established between the new player and the platform;

- flexibility to adapt to different onboarding requirements of entrants.

GSMA keeps upgrading the test platform to cater to the needs of all participants and achieve the set goals.

Everyone who is interested in testing the platform can join the project. Just sign up and follow the GSMA guidelines.

Learn more about the project from our case study.

On a side note

Some of the key insights on mobile money interoperability you may want to take away:

- MMI refers to digital financial services and implies the ability of mobile operators, financial institutions and other service providers to initiate mobile payments between users;

- the adoption of mobile money solutions is crucial for the population and businesses in developing countries like Ghana, Pakistan, India, Peru, etc;

- main benefits of MMI for emerging markets line in combating financial exclusion, decreasing poverty, eliminating the gender gap, developing the national economy;

- every MMI system should be carefully tested for its reliability and robustness.