With the evolution of the crowdfunding and P2P lending, now has come the era of a different ecosystem for funding projects. The benefits of peer to peer lending for startups are not always on the surface since they usually go hand in hand with special pains. In this article, we will cover the advantages of P2P lending for startups and show why it can be good for your business.

P2P lending has already become quite mainstream, and over the past years, we have seen some tremendously successful campaigns that got funded fast in almost no time.

Before we jump into details of the pros and cons of peer-to-peer lending, let’s have a quick overview of what P2P lending is and how it differs from conventional crowdfunding.

What is P2P lending

P2P lending is a way to get money from a number of investors online. The lending process happens on a P2P lending marketplace where borrowers sign up and list their loan requirements and investors get a chance to look through all the available loan listings and decide what they want to invest into.

The loans are typically given for personal needs like house renovation, car buying, debt consolidation, or medical expenses. Such loans range from £500 to £35,000.

Small and medium-sized businesses (SMEs) can also count on getting a loan through a P2P lending platform. If a startup needs extra funding for asset purchase, research and development, stock purchase, expansion or acquisition, it can get a loan from £25,000 to up to £75,000 (sometimes even more).

Since the P2P lending industry is relatively new, pros and cons of investing in peer-to-peer lending for investors include less stability, the risk of losing money if the borrower fails to repay the debt, less liquidity, and no guarantee of profit (loans usually are unsecured).

How P2P lending is different from traditional crowdfunding

The fundamental concept here is that P2P lending is a special case of the crowdfunding model, and the main difference is the funding type.

Traditional crowdfunding works on equity-based investments — for example, equity stakes in real estate. P2P lending is a debt-based investment which presumes that the borrowers repay the loans in several instalments over a set period — usually 1 to 5 years.

The most popular P2P lending platforms are:

- FundingCircle

- LendingClub

- Zopa

- Prosper

- Kabbage

- Upstart

- Earnest

Now let’s move on to the peer-to-peer lending benefits and challenges.

Pros and cons of peer-to-peer (P2P) lending for startups

Let’s talk about all the good things crowdlending has for those companies which are at the starting point.

We will back up all P2P lending advantages with examples from our portfolio so that you can see how it works in practice.

1. Streamlined application process

What makes P2P lending win over a bank loan is a simplified application process. P2P lending platforms provide direct interaction between borrowers and lenders.

Borrowers sign up and describe the purpose of their loan in as many details as possible to make it more clear and attractive to lenders. They can also check the interest rates directly on the website and get an idea of how much they will need to repay.

The platform usually performs all the necessary checks quickly and makes your project available for investing in no time.

Peer to peer marketplaces usually ask for:

- your personal information;

- loan amount;

- your credit score;

- purpose of the loan;

- your income range.

If you apply for a business loan for your startup, you may be asked to give details of your business financials as well as submit balance sheets, tax returns, and profit and loss statements.

Investors also take into account your time in business, revenue and profits, and revenue.

Lending Club provides a quote calculator (and requests quite some data) to give a clear understanding of the amount to be repaid.

Funding Circle has a similar signup process that allows getting your eligibility validated in seconds.

Same is with Kabbage – simple and clear.

Obviously, quick onboarding doesn’t mean that whoever asks for a loan will get it.

P2P lending platforms conduct thorough checks to determine credit-worthiness and will approve businesses with healthy financial track records. One of the disadvantages of peer-to-peer lending is the necessity of higher credit score (as opposed to other crowdfunding models).

An online loan application is considered a soft inquiry and doesn’t directly impact the credit score, but P2P lending platforms pay attention to the number of credit inquiries in the past six months.

CapitalRise

CapitalRise is a crowdfunding site that partners with property developers of prime real estate in the UK. The provider offers a cheap source of capital loans for a variety of property types including residential, commercial, industrial, self-storage, retail and hospitality.

At their FAQs, CapitalRise notes that borrowers must have a comprehensive business plan for the project and detailed development appraisal/investment cash flow to get access to funding.

Plus, the property should be in good locations with strong demonstrable demand.

Only those property developers who are based in the UK with UK bank accounts and meet the selection criteria can be listed on the platform.

To apply, developers fill in the initial information requirement form and further discuss peer to peer lending pros and cons with CapitalRise team.

2. Get funded quickly

The funding speed depends, but it’s highly possible to get your goal completed in 1-2 weeks. Unlike banks where the process can last for weeks on end, peer to peer loans is more transparent.

P2P platforms market their investment opportunity to a big crowd of investors. Since the investment amount can be as little as £10, the number of people who would like to participate is significant. It’s the key factor that helps P2P loans get funded at the drop of a hat.

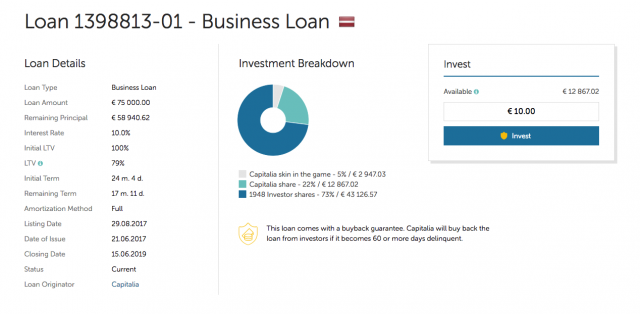

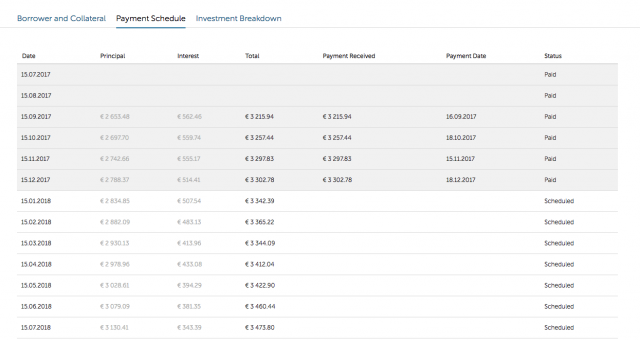

Mintos platform displays vital information about the loan originator and answers many questions before they are asked. They also put an Invest button in a prominent way encouraging to invest right away.

Mintos also lists payment schedules on the investment opportunity listings which builds trust with those who are planning to invest their money.

Even if a loan is rejected by some platform, this becomes known quite quickly, and the borrower can try other platforms to get the funding through.

Homegrown is the provider of opportunities to support established real estate companies for angels and everyday investors specialising in pre-vetted residential and mixed-use development projects.

The company works with mezzanine financing – a blend of debt and equity financing pairing p2p lending pros with equity fundraising benefits.

If you’re eager to try the luck with Homegrown, this is what they offer:

- ability to raise up to 90% of a development’s equity requirement;

- investment size from £200,000 to £6 million;

- fully underwritten funding;

- competitive terms;

- flexible and personal service ;

- liaising with senior lenders.

3. Better interest rates

There are a few ways to determine interest in peer to peer marketplaces.

– The borrower decides the interest rate they want, and the investor estimate whether they want to invest in such a loan. Of course, investors will be more driven by higher interest fees, but if the lender demand is high, the borrower can get funds even with a lower interest rate than they initially set.

– P2P marketplace sets the interest rate according to the requirements it specifies. In this case, credit grade, loan period and other parameters will affect the rate, which will be used for all borrowers with the matching requirements.

– Flexible rates to match demand and supply – the rates may move up or down depending on the recent demand and supply activity.

Again, if we compare with traditional ways to get funding, the interest rates in P2P lending are much lower. The interest is what makes the lender happy.

Just like with online shops, P2P websites don’t have buildings to maintain and administration costs to pay. Hence they can afford more attractive conditions than banks.

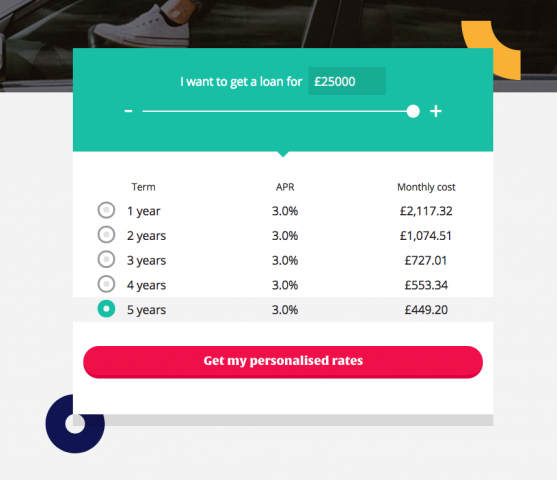

Usually, the platforms show the interest rates right away – Zopa gives this information when you decided to sign up for a loan:

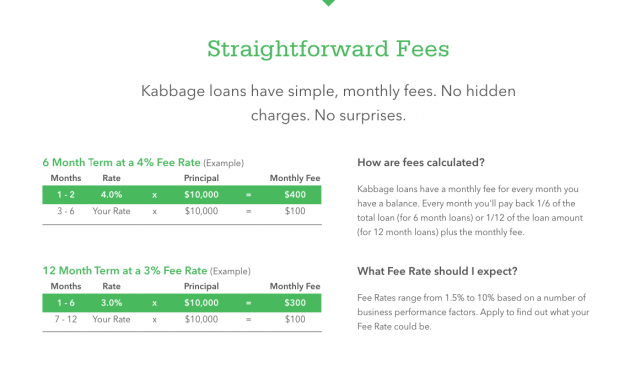

Kabbage explains in detail how fees are calculated:

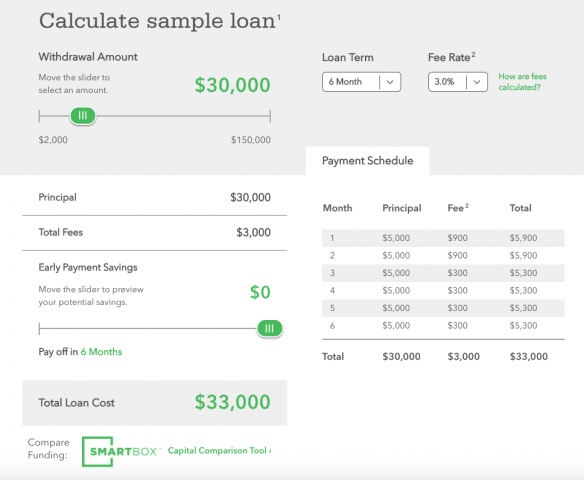

They provide a loan calculator as well and illustrate the payment schedule:

Also, borrowers who have already repaid their online loan have higher chances to get better interest rates when they decided to apply for a second loan.

Take into account that the P2P lending platform charges anything from 1% to 6% of the loan amount for application processing which is called an origination fee.

Glenhawk

Glenhawk is a unique alternative lender providing short-term loans for several types of real estate:

- commercial and semi-commercial;

- residential;

- refurbishment;

- 2nd charge.

The types differ by the goal, loan size, interest rate, term, and arrangement fee. Here’s a breakdown of prices for you to understand p2p lending pros and cons with Glenhawk.

Refurbishment loans to support refurbishment work on any existing structure. Offered for 0.70%+ per Month for 3 – 18 Months.

Buy-to-let is to cover a property purchase. You can get it for a period of 3 – 18 months at 0.65%+ per month.

2nd Charge bridging loan is a quick way of capital raising, independently of the principal mortgage. Terms: 0.75%+ per month; 3 – 18 months; max loan to value – 70%.

Commercial loans are to help you acquire property or get funding for redevelopment works. Available at 0.70% per month from 3 to 18 months.

4. Quick access to funds

Money can be used immediately after investments start to come. Interest is only paid on the funds used, so the amount can sit there until it’s needed.

Besides, there is no obligation to take funds at all so if something has changed along the way there is no need to repay anything.

The platforms usually provide a convenient way to access funds through a mobile application or desktop. The borrower can choose the amount to be taken, review the repayment schedule, and get the money transferred to their bank account within 1-3 business days.

Repayments are also managed quickly and can be consolidated into one monthly payment, so there is no need to remember all payment schedules.

Shojin

Shojin is a property investment company based in London with an online platform making property investments accessible to the general populace.

How the Shojin crowdfunding model works for developers:

- Submit a project for a review on the platform if you feel Shojin Property Partners may be interested in (the company works as a co-investor).

- Once it’s reviewed, the team will issue an offer letter in case your project is suitable for the provider.

- Submit all supporting documents and undergo full due diligence.

- Shojin approves the project and issues formal terms.

- Once the terms are agreed by both parties, the project is listed on the platform.

Check Shojin guide and find out peer to peer lending pros and cons for yourself.

5. Unsecured loan – no collateral

This disadvantage of peer to peer lending for investors is an advantage for borrowers. Not all of the P2P lending platforms allow loans with no collateral and not all investors will agree to risk their money investing in such loans.

However, the platform requires a certain credit score and verifies eligibility by other parameters, and it might take collateral lightly and drop it from the requirements.

Cashflow is taken into account too, so if you have an established business, you may get away without any collateral.

Despite being a bailout for startups and small businesses, P2P lending presents some challenges for them.

For instance, CapitalRise creates bespoke security packages for every single loan they fund.

A security package will typically include:

- Legal Charge. CapitalRise has a legal right to sell a property if a borrower is unable to repay a loan;

- Debenture. A debenture creates a fixed charge over Land and Buildings registered in the name of the borrower in England and Wales and a floating charge over all assets not already charged;

- Personal Guarantee. A personal/corporate guarantee from the borrower or property owner that equals 20% – 25% of the total loan;

- Collateral Warranties & Step-in Rights. In case of the borrower’s default, CapitalRise could ‘step-in’ and maintain existing contracts.

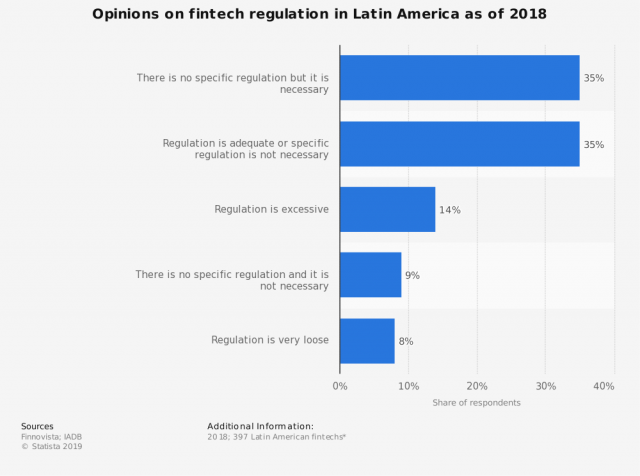

Insufficient regulatory framework

Alternative lending is growing faster than the global legislation system can tear it down.

Most of the countries still don’t have enough regulatory basis for controlling relationships between the borrower and lender in the P2P sector.

Some governments monitor only specific areas while others strive to improve the current framework to adjust the needs of both parties.

It greatly influences the demand for P2P lending services as lots of businesses don’t find this fundraising method very reliable and turn to traditional loans.

The UK is the front-runner in the crowd. The FCA whose priority is to control peer-to-peer lending for startups has placed huge efforts to protect the rights of both parties.

In its recent report, the body suggests that platforms take more care of their clients by providing less risky services.

This is exactly what the young P2P lending market needs.

Lack of personal communication

Given that all interactions take place on crowdfunding websites, borrowers and lenders do not meet face-to-face.

On the one hand, it may not appear to be a big problem for companies. On the other hand, you never know who to shake hands with in gratitude for the support.

According to a survey, the lack of social interactions in the P2P lending process has a huge impact on the chances that a startup won’t be able to get a project fully funded.

In the past, some crowdfunding companies had social groups where clients could build personal communications.

Within these groups, potential borrowers could get advice on how to create a successful campaign, quickly raise funds, and even meet potential investors.

However, most of the communities are closed today and the issue of insufficient interactions still exists.

Small-scale fundraising

Another limitation of peer-to-peer lending for a business startup is small amounts of money that can be collected.

One of the original benefits of P2P lending was bypassing pitfalls small businesses encounter on their way to raise seed capital.

Unlike large corporations, small entrepreneurs have fewer chances to find a professional backer wanting to invest a couple of bucks. And banks simply don’t have a strong desire to collaborate with them.

On lending sites, handfuls of cash the crowd is eager to donate form relatively small credit pools that can be used to achieve unpretentious business goals.

Thus, if your idea is estimated at lots of money, then, probably, you should consider traditional loans.

Bad credit scores paired with high interests

The last but not the least. Crowdfunding companies take big risks when dealing with inexperienced borrowers.

To protect backers, they set high return rates on non-performing loans in their portfolios.

The loan category is defined according to the credit-worthiness of a borrower. So, if you hope to get cash for very little interest, consider your credit rating first.

For those with an imperfect story, the price of raising funds may be too high and unbearable in the long run.

Note, that if you fail to repay a loan, it may dramatically impact your status as a borrower and reduce the chances of getting future loans.

Extra peer to peer lending advantages and disadvantages

✅ no need to deal with several institutions, everything is done via a single platform;

✅ since loans are unsecured, they can be more flexible;

✅ free quotes from platforms don’t affect your credit score;

✅ the platform offers professional marketing tools to promote your project;

✅ new contacts among angels and industry players.

❌ shorter terms and more frequent payments;

❌ additional arrangement fees;

❌ sometimes cash is slow to get lent out.

Bottomline

P2P lending for startups is an excellent alternative to a traditional loan from a bank and is well suited for small businesses and startups.

Advantages and disadvantages of peer to peer lending are numerous and better be evaluated and weighed out before jumping into it.

Advantages include a quick online application, unsecured loans, fixed monthly payments, checking rates without affecting the credit score, lower interest rates, fast access and flexible use of money, no early payment fees.

Disadvantages are mainly focused on your eligibility. Interest rates may be higher if the credit score is below average, P2P marketplaces charge quite high origination fees against the loan amount (up to 6%), missed payments may have the negative impact on your credit score.