You have got an early-stage business, and you’re looking for a financial backup for its further development?

Decades ago you would beat down the door of every bank to get loan approval. If you hadn’t succeeded, you would have had a chance to interest other investors, though.

However, this exhausting process of raising funds often reached a dead end anyway.

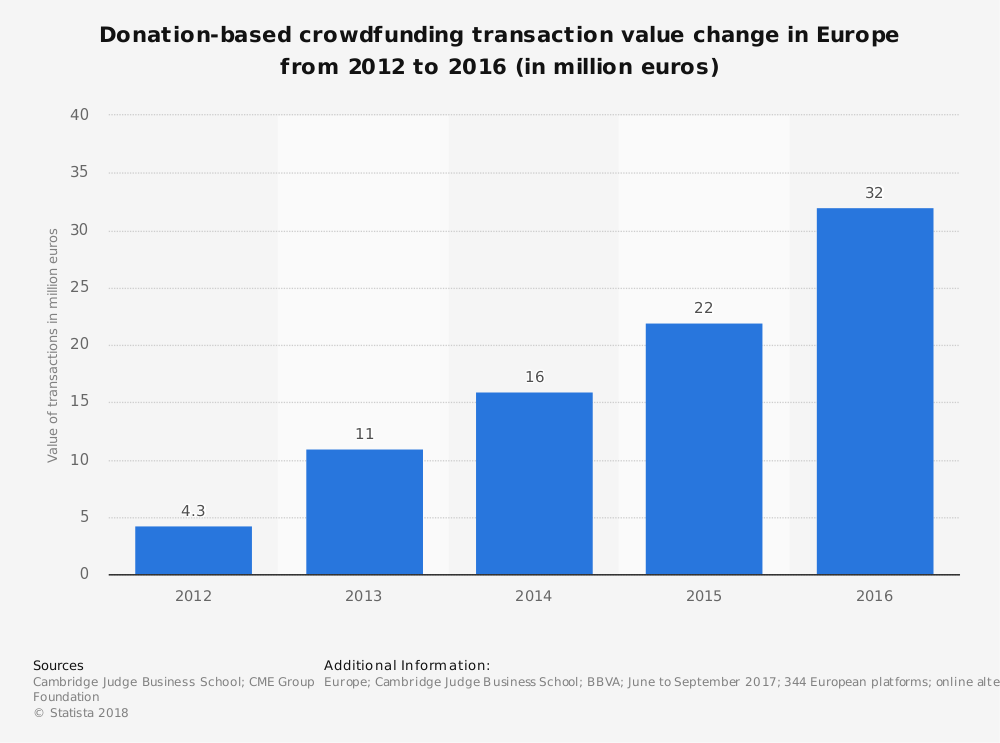

The sharing economy and progressive technologies have given the world an exciting thing – alternative financing. It has two types – crowdfunding and peer-to-peer lending.

Despite being the opposite, they are often mixed up. This fact sometimes is the reason for their inappropriate usage in a business environment.

Today we’re going to clear the air and find out what is the difference between crowdfunding and P2P lending.

Crowdfunding in a nutshell

It’s not by accident that the term “crowdfunding derives from the words “crowd and “funding.

The concept of crowdfunding is straightforward – every little bit helps. Investors, aka sponsors or donors, combine efforts to assist in launching a project. Of course, it’s all about financial assistance.

Thanks to numerous crowdfunding platforms, the whole deal doesn’t take long, which is crucial for emerging businesses.

Unlike bank loans, startups don’t have to make monthly interest payments.

In equity- or reward-based crowdfunding, they can offer a stake in their company or a part of the final product in return for financial infusions made in advance.

There are various crowdfunding platforms in the market that specialise either in equity deals or reward patterns.

First, entrepreneurs offer their projects for a review and, if approved, their proposals become available for potential investors.

Then the process of fundraising starts. Once all the interested sponsors have made their contributions, a company receives the money on its account in a beneficiary bank.

Whether or not investors reap the benefits depends on the success of a project.

International P2P and crowdfunding legislative framework

Given that debt-based and equity investing are quite new forms of alternative financing, the regulatory system for such relationships is still developing.

The UK is one of the pioneers striving to design a unified system for regulating this segment of the financial market.

Loan-based and investment-based crowdfunding platforms are under the control of the Financial Conduct Authority (FCA).

Recently the regulator suggested that P2P platforms make changes in their business models in order to prevent investors from taking sufficient investment risks.

These recommendations include:

- strengthening requirements for borrowers;

- P2P business models optimisation;

- enhancements in staff training to increase the overall level of competence;

- improvements in risk management practices;

- limitations for particular types of investors;

- full disclosure or the role of a platform.

Likewise, FCA proposed amendments in the activity of investment-based providers, in particular, the mandatory assessment of an investor’s certified status.

In the US, it is the Securities and Exchange Commission (SEC) who controls the crowdfunding market.

The key requirements SEC imposes to crowdfunding dealers are:

- a compulsory platform registration in the SEC and FINRA;

- the maximum amount of securities issued within a crowdfunding campaign;

- limitations of investment amounts and securities sale;

- disqualifying precautions.

Australian crowd-sourced portals follow the guidelines created by the Australian Securities & Investments Commission ASIC.

In general, the CSF legislation concerns the registration process, risk and conflicts of interest management, resource requirements, and disclosures.

However, there are still lots of issues waiting to be covered in the guidelines and templates.

Canadian security regulators made the first attempts to adapt their law to new forms of financing in 2015.

The National Crowdfunding Association of Canada (NCFA Canada) regulates only equity investing as it is the only form of fundraising that implies the securities issuance.

The NCFA policy specifies offering limits, types of securities, issuer and investor limitations, software requirements, etc.

Different shapes of crowdfunding

You have made a decision to kickstart your business idea with a helping hand of crowdfunding.

All right, what’s next?

Reward-based, donation-based, equity or, maybe, debt crowdfunding – which way to choose?

Remember, there is no “one-size-fits-all solution and you need to carefully weigh up all the pros and cons before selecting the right one.

1. Equity crowdfunding

Probably, you already know what equity crowdfunding is.

When purchasing a share in an enterprise, investors look forward to obtaining a financial benefit. This allows considering equity crowdfunding as a conventional investment project in industries such as real-estate.

If the business turns out to be successful, the investors will be pleased with the outcome as their shares become more valuable.

Otherwise, their stakes will be worth nothing. Of course, for investors, some risk is always there, and sometimes it’s worth taking.

If you’re about to start investing in real estate, learn the key benefits and you will get as an investor.

2. Reward-based fundraising

It’s not quite correct to call investors those people who make financial injections in exchange for a reward.

In fact, they act as sponsors, donors or patrons, if you wish.

That’s why reward-based financing is not an investment. If you volunteer to help such a project, you can hope for a bonus like a free product or service.

Typically, you can get it in several months.

There are some websites which deal only with reward-based donations like Kickstarter or Indiegogo. So, if your project is good enough for the crowd, you can showcase it on one of them.

3. Donation-based financing

According to Investopedia, donation-based crowdfunding supposes that a lot of backers contribute to one project and receive token-rewards for it.

The value of returns is directly related to the amount of donation. In return for small-sized contributions, sponsors may not receive any reward at all.

Token donations may come about in a wide range of forms, most commonly being pre-sale items. As the nature of donation-based crowdfunding is similar to reward-based one, they’re often correlated.

This way of raising capital works well for charitable and social purposes.

4. Debt crowdfunding

Debt crowdfunding – what’s it all about?

The notion is a bit different from the rest. However, it’s still related to crowdfunding forms.

Debt crowdfunding is also known as crowdlending. It’s not a surprise that the term ‘lending’ in this definition changes the idea of investing money for loaning the same.

Multiple creditors give small loans to a borrower via a crowdlending platform. In return, they expect monthly payouts just like in a typical pattern with bank loans.

However, crowdlending is free from unnecessary hurdles you can face when dealing directly with banks.

Debt crowdfunding can take two forms – P2P and P2B lending. We’ll talk about them later.

Pros & cons of crowdfunding

Both startups and investors love the idea of raising funds through a crowd. Let’s see what makes it so unique.

Can crowdfunding help your business grow?

It’s hard to count the number of advantages that businesses can find in crowdfunding.

Amongst the major ones are:

- Time & money saver. We are used to saying that time is money. Crowdfunding allows implementing business ideas faster and more efficiently.

- Access to funds. As opposed to conventional go-betweens, crowdfunding gives businesses unlimited financial perspectives. Rather than wasting your time negotiating and convincing, make and realise your business strategy.

- Rewards control. Voting for crowdfunding, you get total control over your payments. It’s you who decide how to honour investors – with material benefits or token rewards.

Challenges of crowdfunding for startups

However, not everything is as smooth as it seems to be. Crowdfunding sometimes is not suitable for:

- Complex strategies. It doesn’t work with them, unfortunately. Being great for small-sized business visions, it can ruin larger ones with lengthy research-and-development stages.

- Substantial capital needs. Usually, platforms work with projects requiring less than $100,000 of seed capital. Larger projects should opt for banks.

- Flexible projects. Once you’ve collected the money, you can’t change your offer, the pace and time of payments in particular.

Benefits of becoming a crowdfund investor

If you are an investor, crowdfunding also has something to offer you:

- Deliberate choice. Usually, an investor knows who they are going to help as all the projects are exposed on the platform. It makes investing ideological as well as financial.

- Lack of volatility. Crowdfunding market doesn’t undergo economic fluctuations as it’s not linked to other financial markets.

Crowdfunding investing risks

Also, there are still some risks for investors:

- Win-win or lose-lose. As the largest part of projects is presented by startups, you never know how things will be developing. Prospects may be promising and seductive, but remember that a large part of business ideas fail.

- Equity or debt? Some risks of crowdfunding are caused by the nature of investments. While equity deals continue to promise more benefits, debt investments are less risky.

Top crowdfunding platforms

Crowdfunding would be an empty word if there were no specialised platforms whose business is to bring startups and investors together.

The marketplace is flooded with companies for every taste. All the sites are nominally divided into two big groups – P2P or crowdfunding.

The platforms from the first group focus on reward- or donation-based investments. The others serve as equity-based crowdfunding providers.

We’ve already mentioned two solid platforms of the first type – Kickstarter or Indiegogo. However, they are not the only ones.

A specialised business sector is also represented by PledgeMusic, Speed&Spark and Barnraiser.

Let’s say, you’re willing to try equity fundraising.

There are so many options in the market that you may find yourself in analysis paralysis! Every broker from Angel List to RocketHub has its features and might be a perfect fit just for your case.

Real estate crowdfunding is gaining momentum now even amidst the COVID-19 crisis.

For example, CapitalRise is a London based property investment company with a platform for supporting high-end property developers.

It’s one of our valuable projects from the RegTech portfolio that’s been quite successful on the market. CapitalRise carries out extensive due diligence of the property development projects published on the platform and boasts a reliable reputation. Some of the investment opportunities get funded within less than 24 hours!

We’ve already shared our view on how to build the best crowdfunding platform for startups.

The input of fundraising companies into the economy can hardly be overestimated, and the number of successful projects is the best illustration of this.

Below you’ll find some examples.

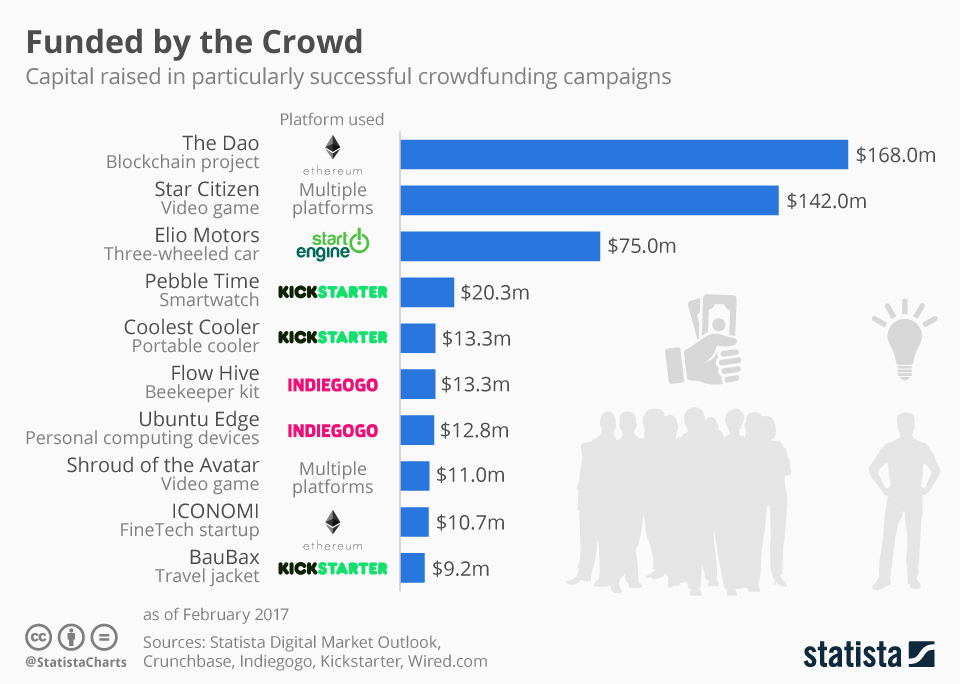

Successful crowdfunding campaigns

- The Pebble E-Paper Watch – an amazing Kickstarter’s breakthrough in the crowdfunding marketplace. It has been known to have collected a large sum of money (over $10m) in less than 40 days.

- Pono Music – another “brainchild of Kickstarter with a focus on musical experience. More than $6m was raised in just a month to provide an exceptional musical experience for users.

- Bitvore – a firm specializing in big data analysis. Their campaign was launched in Fundable and will be remembered for gathering $4m+.

- Canary Smart Home Security – Indiegogo helped these guys to raise $1.9m in just 34 days to create a device used for home security with super powerful features.

This list goes on and who knows, maybe, you will be the next memorable crowdfunding project!

Why is crowdfunding good for your business?

Crowdfunding breaks “the stereotypes of good old investing as it makes it easier, faster and more exciting.

At the very moment it appeared, business-minded people had a sigh of relief.

Crowdfunding market hasn’t stopped surprising the crowd. Every day new inventors get a chance of making their business dreams come true, and investors can become their “fairy godmothers.

The impact of crowdfunding on people, businesses and the global economy is tremendous.

Crowdfunding vs. P2P lending platform: what to choose

Picking the right fundraiser isn’t as easy as choosing a film for tonight.

First off, decide what model you’re gravitating towards more – p2p lending or crowdfunding.

To an end, consider your niche and the business specifics, think about desired roles for investors and how you can prove your business concept.

Despite the difference between crowdfunding and peer-to-peer lending, both and their combo (e.g. mezzanine loans) work better than traditional schemes. Although, it’s hard for incumbents to admit it.

CapitalRise, for example, prepared a guide with 10 questions you should ask yourself before opting for a crowdfunding company.

Things to consider in brief:

- FCA authorisation;

- the platform team background and expertise;

- investments risks;

- testimonials and the quality of client service;

- CDD requirements and security of assets;

- tax benefits and fees;

- portfolio diversification.

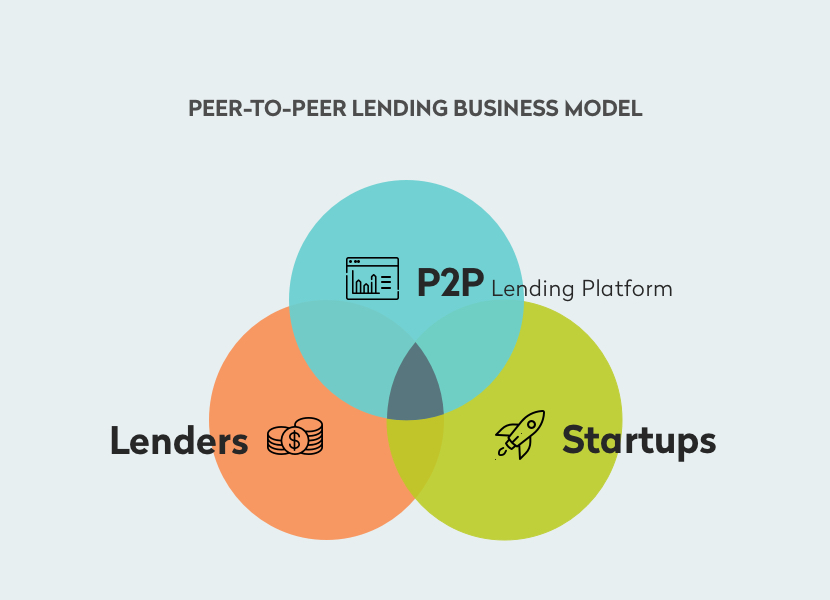

What you need to know about P2P lending

In the aftermath of the global financial crisis, banks began losing their monopoly on a financial market.

The main reason for this was a dramatic fall in client confidence. Another one – limitations on credit financing.

As a result, borrowers began looking for innovative financing, and peer-to-peer lending started to grow in strength.

The concept of p2p loans is fundamentally different. A network of individuals or companies lend money rather than invest it.

Peer-to-peer lending tends to be more in favour of investors as it comes with far fewer risks than equity investing.

Many P2P lending sites claim that they accept only solvent borrowers.

That means investors funds are in the safest place.

The lender earns profit via interest payments; they don’t purchase any shares or stakes. Some peer-to-peer lending providers offer creditors to sell out their financial rights.

In this case, they earn money at a lower rate determined in compliance with the actual duration of the investment.

Another thing worth mentioning – investors’ income from peer-to-peer loans is tax-free, which is very attractive to investors too.

Just as in a crowdfunding model, three parties are participating in peer-to-peer lending.

The overview of P2P lending forms

Earlier we mentioned that peer-to-peer lending is debt crowdfunding, to be exact.

Mainly, it has two distinct forms – P2P and P2B lending.

As you can see, the terms differ only by one letter, but this is important.

Let’s see what the difference is.

P2P loans enable people to lend cash to others using special online portals.

As a result, tiny pieces of investors’ funds form a large loan to be given to a borrower afterwards. It’s essential that banks are not invited to participate in deals.

This helps avoid bureaucracy, which everyone hates, and makes the lending process fast and easy. Another nice perk is higher interest rates that pledge mind-blowing income.

P2B loans enable anyone to finance enterprises. When applying for a presence on a lending platform, businesses provide basic information about their projects: a concrete purpose of raising funds, financial statements, crowdfunding strategy etc.

A person can review a business portfolio and select a project they are keen on.

A lot of sites deal with both P2P and P2B lending proposals, however, actually, they deal only with the first type.

If you feel more than willing to participate in P2B lending endeavours, you can try Funding Circle or Nucleus.

The benefits & challenges of P2P lending

As it always happens, there are positive and negative things about P2P lending.

No matter who you are in a deal – either borrower or a lender, you should consider the benefits and risks of P2P lending before making a decisive step.

Is P2P lending right for your business?

- You might remember those unbelievable annual interests offered by banks. P2P loans, in contrast, typically don’t oblige debtors to spend much on fundraising.

- P2P lending is a web service which means the application process occurs in a blink of an eye. It makes you forget about the tedious paper routine and hours of waiting.

- Unlike bank loans, P2P lending doesn’t require borrowers to pay penalties if they want to pay off a loan in advance. Also, there is no need to provide any collateral for a loan.

- Thanks to the transparency of online portals, startuppers can view what progress has been made in fundraising and who has contributed to a project.

The risks you take as a borrower

- Sometimes it’s not so fast and easy to create your portfolio as it depends on your crowdfunding strategy.

- As the P2P lending market is not so liquid as other financial markets, the opportunities you offer might give way to other financial instruments.

- Online platforms prefer creditworthy borrowers. So, if you have a lousy track record, you may lose your chance.

- There is one common thing between P2P platforms and banks – you must fulfil your duties. If for whatever reason you can’t do it, it will severely affect your reputation.

Is peer-to-peer lending a good investment?

The perils and profits for investors:

- Both people and corporate investors can make contributions.

- A simple and quick way to open an investment account – $25 is enough for an initial contribution.

- A great way to make your portfolio well-diversified and earn a steady income.

- You decide yourself who you want to support and why.

- There is still some risk of losing money due to the presence of dishonest borrowers on a platform.

- Getting a return takes some time, so if you’re planning to get instant income, this way is not for you.

A close look at the P2P lending market

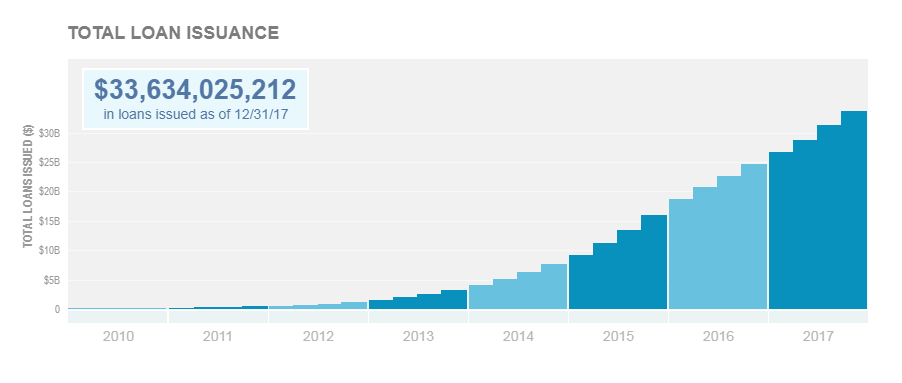

With more and more P2P lending providers appearing in the market, it becomes more available for almost everyone.

The amount of P2P loans issued by these sites has been growing and, as it’s projected, this tendency will remain the same.

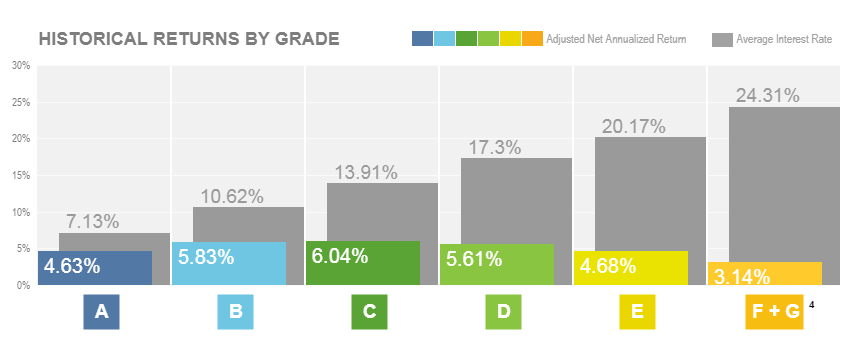

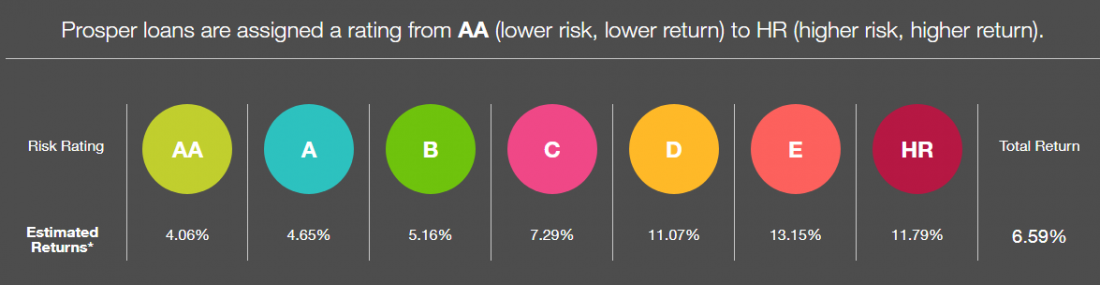

However, if you ever decide to dive into P2P lending, you will find out that there are mature players like Lending Club or Prosper which have already found their place under the sun.

With long experience and a solid reputation, they occupy almost the whole marketplace.

These portals deal with a wide range of projects with different budgets, strategies, needs and features. There you can find an investment opportunity to every taste.

Source – prosper.comThere are smaller platforms as well – Peerform, FreedomPlus, SoFi and many more.

So, if you feel that you’re not ready to make serious investments or your project is not good enough for bigger platforms, you can start with these smaller options.

Two of our customers, Glenhawk and InvestMySchool, provide startups and enthusiasts with access to the loan market.

Glenhawk deals specifically with real estate projects. The company raises funds for commercial and semi-commercial, residential, refurbishment, 2nd charge.

Recently, the company has extended the range of its financial products. If you’re seeking financial help to elevate your property project, consider Glenhawk’s bridging loans (residential or commercial), refurbishment and 2nd charge mortgages.

InvestMySchool is the first UK based crowdfunding platform for independent schools. The company fundraises with donations and P2P loans for schools and educational organizations.

Borrowers set the interest rates themselves and decide who they would like to receive funds from.

Any UK citizen aged 18+ and holding a UK bank account qualifies to register with InvestMySchool.

InvestMySchool has two repayment modes: term and bullet methods.

How does P2P lending benefit the business?

P2P lending is a perfect alternative to investing. With its help startups can gain the necessary funds for growth in a short period without significant efforts.

P2P lending has some advantages: less paperwork and lower interests, fast application procedure and more lenient requirements.

However, borrowers and lenders may face some challenges: lack of rules regulating P2P lending, the minimal collaboration between parties, higher investing risks.

Despite these drawbacks, P2P lending continues to increase the momentum and soon might displace traditional bank lending from the market.

The difference between P2P and crowdfunding: extra use cases

Knowing the merits and limitations of crowdfunding vs. peer-to-peer, why not to embrace both?

This is what CapitalRise and Shojin do.

At the CapitalRise platform, you can choose between debt and equity.

There are 2 types of debt products — interest-bearing bonds and deep discount bonds.

The difference lies in how the return on the investment is classified which affects whether CapitalRise needs to withhold tax when making repayments.

By investing in equity products, investors buy shares in the SPV. When the property is sold and the investment ends these equity investors will receive their capital repayment and their share of the profits.

Shojin combines equity and loans in mixed products like mezzanine loans.

It’s a great option for those who prefer investments with fixed returns which are secured by an underlying asset within longer timescales.

Alongside mezzanine products, Shojin offers bridge loans, asset investments, and lifestyle corporate bonds.

The last suits investors wanting flexibility.

You invest in Shojin at company level and can choose from various options, including monthly or annual income and short or longer loan terms.

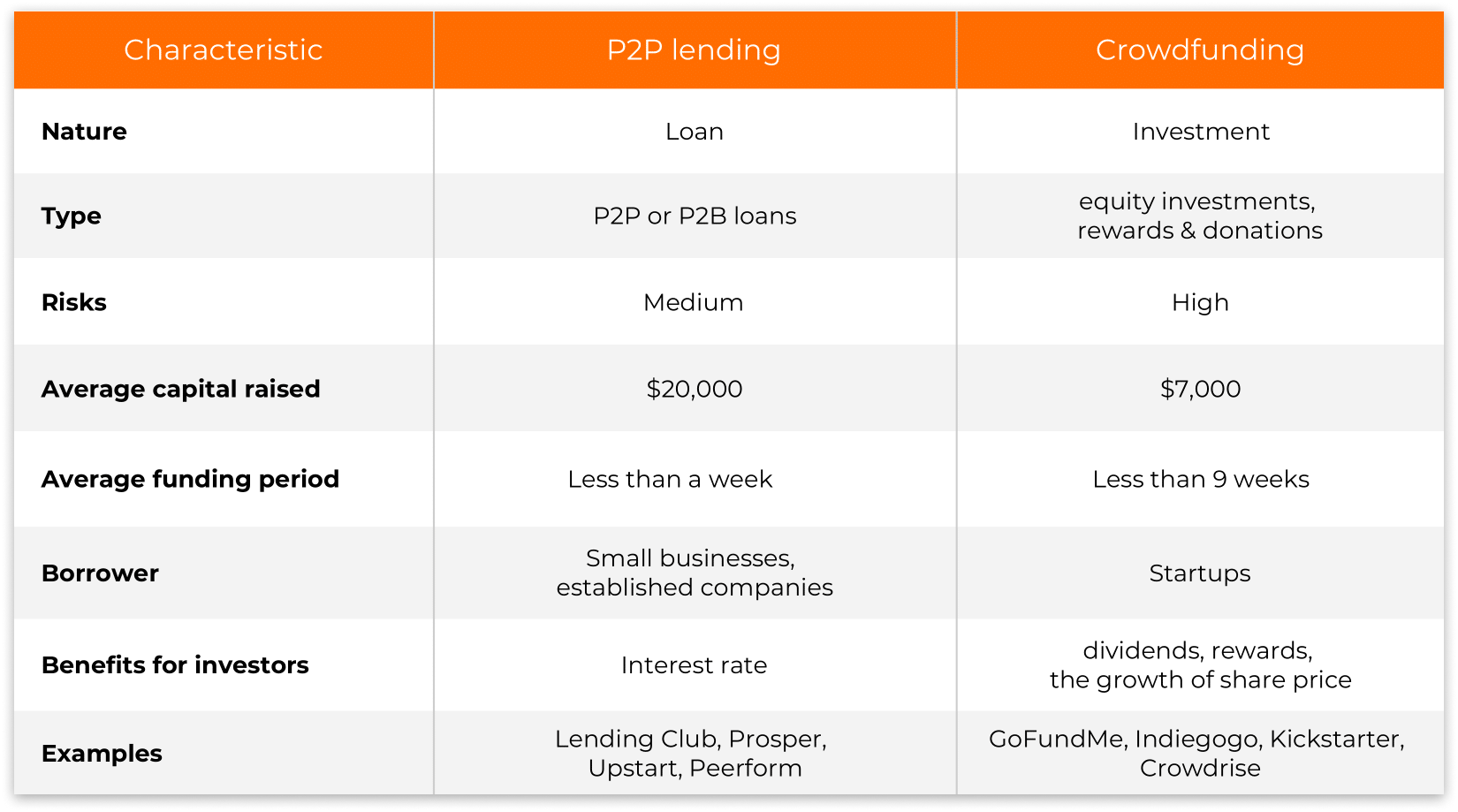

Crowdfunding vs. peer-to-peer lending

Grounding on the review on alternative fundraising, let’s sum up what we have got.

Here’s what it boils down to:

- Crowdfunding in its classical forms has more risks than P2P lending. It requires investors to make well-informed decisions more sophisticated. This model is diverse and offers different financial schemes like donations, rewards or equity deals.

- P2P lending is less dangerous and gives more explicit promises on returns. However, it compels borrowers to fulfil their obligations earnestly.